Will mortgage rates fall if the GSEs buy $200 billion of MBS?

If Fannie Mae and Freddie Mac materially increase their purchases of mortgage-backed securities (MBS), the most likely impact is modest downward pressure on mortgage rates. The effect is limited, uneven, and conditional on broader market forces.

Transmission Mechanism:

When GSEs buy more agency MBS, demand for those securities increases. This pushes MBS prices higher and yields lower, which compresses the primary–secondary spread for mortgage lenders. Lenders can then offer slightly lower mortgage rates to borrowers. This mechanism is similar to quantitative easing, though on a much smaller scale.

Expected Magnitude:

Historical experience suggests mortgage rates could fall by approximately 5 to 25 basis points (0.05%–0.25%), with most estimates clustering around 10–15 basis points for a program on the order of $200 billion. This is noticeable but not dramatic.

Why the Impact Is Limited:

The agency MBS market is very large, roughly $9–10 trillion, so even a $200 billion purchase program represents only a small share of outstanding securities. Treasury yields still play a dominant role in mortgage rate determination, meaning rising Treasury yields can offset the benefits of GSE buying. Additionally, banks and the Federal Reserve are not expanding balance sheets, limiting the overall effect.

Secondary Effects:

Potential positives include narrower MBS spreads, improved rate stability, and better lender confidence. Risks include perceptions of political interference, which could raise term premiums elsewhere, and concerns about prepayment risk among investors.

Net Assessment:

The base case is small but real rate relief. In the best case, mortgage rates could improve by 15–25 basis points if macro conditions are favorable. In the worst case, GSE buying merely prevents rates from rising further.

Bottom Line:

Increased GSE MBS purchases are best viewed as a cushioning tool rather than a transformative policy. They can modestly lower mortgage rates, especially when Treasury yields are stable or declining, but they are not a game-changer for the mortgage market. (more…)

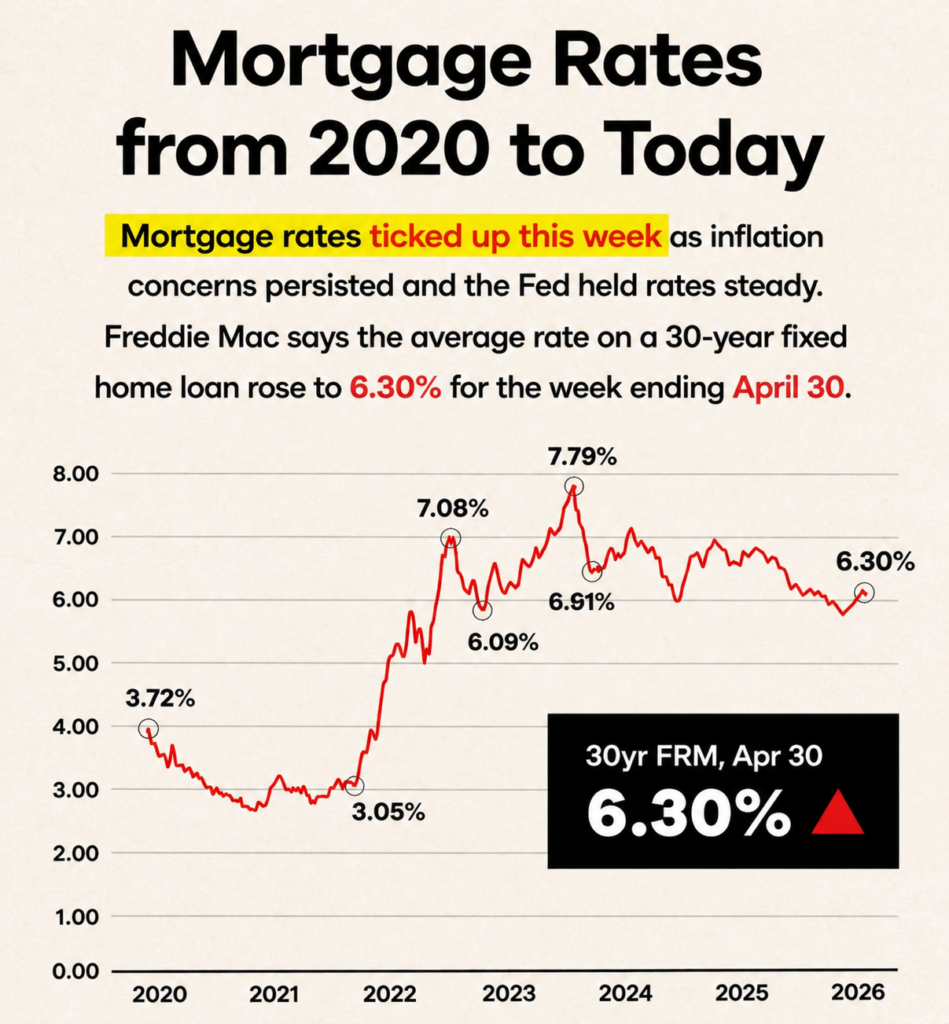

Are mortgage rates holding back the market?

I get asked this question regularly. The chart below covers the last 3 years, and shows that since September 2022 the 30-year FRM has been mostly between 6% and 7% with 3 spikes over 7%, and one drop to 6% in the fall of 2024.The current rate of 6.5% is in the middle of the range for most of the last 3 years.

Politics, Financial Markets, and The Magnificent Seven

At the end of The Magnificent Seven (1960) Yul Brynner says: “…only the farmers won. We lost. We always lose.” (The “we” refers to the gunslingers hired to protect a Mexican village from bandits.)

I am reminded of this quote whenever politicians try to take on financial markets – the markets are the farmers, and the politicians are the gunslingers.

Let us look at two recent examples – I asked my best buddy ChatGPT for non-political commentaries.

UK 2022

When Prime Minister Liz Truss announced large, unfunded tax cuts in September 2022, it triggered a sharp loss of confidence in the UK’s financial markets. Here’s a non-political explanation of what happened and how it was resolved, focusing purely on economic and financial mechanisms:

What Happened:

1. The Announcement:

In late September 2022, the UK government (under PM Liz Truss and Chancellor Kwasi Kwarteng) announced a “mini-budget” featuring around £45 billion in tax cuts — the largest since 1972 — without detailing how these would be funded.

2. Market Reaction: (more…)

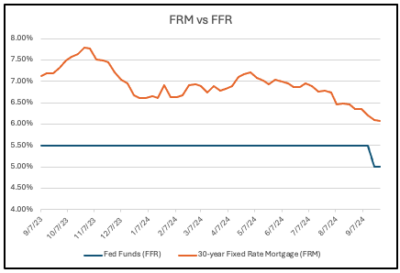

What drives Mortgage Rates – and no it’s not the Federal Reserve

I am always astonished by the number of reports I read, before and after the Federal Reserve (Fed) makes a change in its interest rate, about the effect such a change will have on mortgage rates.

No doubt it came as a surprise to those writers when there was virtually no change in the Freddie Mac weekly survey of mortgage rates this week.

Myth

“Mortgage rates react to the Fed.”

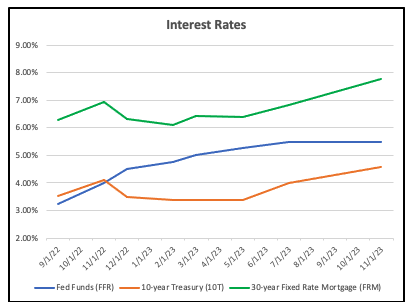

Look at this chart for the last year:

The FFR rate was unchanged at 5.5% for over a year until last week, but during that time frame the FRM varied between a high of almost 7.8% last October and a low of just over 6% last week before the Fed cut its inetrest rate by 0.5%.(The Freddie Mac survey takes place from Monday-Wednesday each week, so the 6.09% reported on September 19 reflected rates before the Fed cut its interest rate).

What happened after the Fed cut rates?

Precious little. The rate before the Fed cut rates was 6.09% and afterwards…. 6.08%.

In simple terms, there is no correlation or link between the Fed’s interest rates and the rate on 30-year Fixed Rate Mortgages.

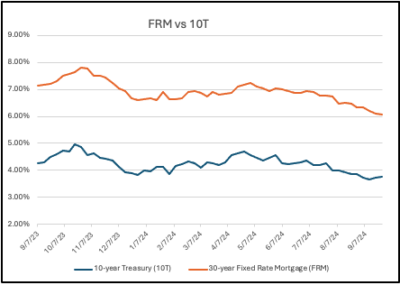

What does determine Mortgage Rates?

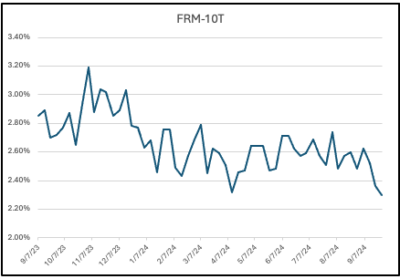

Take a look at this chart which compares the FRM with the yield on the 10-year Treasury note (10T).

Note that the two charts follow each other closely.

Why do Mortgage Rates track the yield on the 10-year Treasury?

Most conventional mortgages (i.e.those meeting the terms set by Fannie Mae and Freddie Mac) are sold by the originator to Fannie and Freddie, thereby freeing up the lenders’ capital to make more loans. Exactly why Fannie and Freddie were founded.

And what do Fannie and Freddie do with these loans? They package them into large pools and sell them to investors in the public market as Mortgage-Backed Securities (MBS). Because investors demand a higher yield to buy MBS than they would to buy a Treasury Note – because the risk is higher – they demand a premium – or spread – above the yield they would receive from the Treasury Note with a similar maturity to the expected life of the mortgages – and that is the 10T.

Is the spread consistent?

Good question. The answer is no.

For most of this century the spread was in the 1.6 – 1.8% range and averaged around 1.75%. The exceptions were:

2008 – the Great Recession and the height of the foreclosure crisis making mortgages unattractive to investors, who demanded higher yields

2020 – at the outset of the pandemic, amidst widespread uncertainty, spreads widened before the Fed started its huge program of pouring money into the economy, buying both Treasuries and MBS and igniting an asset boom

2022-23 – when the Fed finally, belatedly, stopped injecting liquidity into the system, the market reacted to two main factors: the Treasury would need to sell a lot more Securities to fund the spending, and the growing Budget deficit; and the biggest buyer of Treasuries – the Fed itself – was switching from being a buyer to a seller.The Fed also continues to hold a huge amount of MBS, which it is slowly reducing by not reinvesting.

Fannie and Freddie have increased fees to lenders

In addition to the fact that the Budget deficit continues to increase, while the Fed has been a seller of Treasuries, Fannie and Freddie have increased the fees they charge to lenders. These two factors have combined to increase the spread to more than the historic 1.6-1.8% , as shown in this chart, again for the last year:

Where are Mortgage Rates headed?

Thw two biggest questions facing the Treasury market are: will Congress take steps to rein in the soaring Budget deficit, and will foreign investors retain their appetite for US securities?

I don’t know, but to know where mortgage rates are headed,the most important number to watch is the yield on the 10-year Treasury Note.

Cheaper Mortgages are available

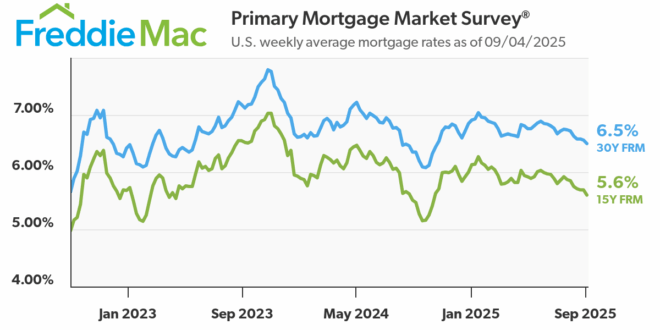

The Freddie Mac weekly survey is a national report. I work with lenders in both Florida and Massachusetts who are offering 30-year FRM for 5.5%. And other options are as low as 5%. Call me for details.

Recent Market Reports

Naples Mid-Year 2024 Market Report

Bonita Springs Mid-Year 2024 Market Report

Fort Myers Beach Mid-Year 2024 Market Report

Please contact me for a market report that includes properties in your area which were recently listed or sold.

Economic and mortgage commentary

The Federal Reserve’s new buzzword: Recalibrate

Federal Reserve Chair Powell:The Time has Come

Earth to Federal Reserve: What are you waiting for?”

The Federal Reserve’s Analysis Paralysis

Andrew.Oliver@Compass.com

The Federal Reserve’s new buzzword: Recalibrate

At Wednesday’s press conference after the Fed – finally – cut rates by 50 basis points (bp)(0.5%) – Fed Chair Powell introduced a new phrase to explain their action: “recalibrate.”

We have been through “transient inflation”; “data dependent”; “higher for longer”; and “data-dependent, not data point dependent” and have reached “recalibrate”.

Chair Powell denied that they were playing catch up because they waited too long to start cutting rates (they are, and they did).

Frankly, after their slow and deliberate approach this year, I expected only 25 bp. BUT…the next meeting is not until November 6, the day after the Election. And who knows what the environment will be on that date? It is certainly not out of the question that there will be a lack of clarity about the outcome. And while the Fed states that it not influenced by political considerations, they will naturally be aware of an environment which may well make it difficult for them to make an accurate forecast of the future.

So 50 bp now is “not a catch up” – but it would have been more consistent – and raised fewer questions – if they had cut 25 bp in July and a further 25 bp now.

Mortgage rates

I will update my 2023 article Why Mortgage Rates will fall in 2024 in the next few days. In that article I predicted that the 30-year Fixed Rate Mortgage (FRM) would drop below 6% by the end of 2024. I also explained why mortgage rates do not follow the Federal Reserve’s interest rate decisions, but are market driven based on the yield of the 10-year Treasury.

And to make to make that point more clearly: in both Massachusetts and Florida it is already possible to get FRMs for 5.5%, a sharp drop from from earlier in the year.

Recent Market Reports

Naples Mid-Year 2024 Market Report

Bonita Springs Mid-Year 2024 Market Report

Fort Myers Beach Mid-Year 2024 Market Report (more…)

Federal Reserve Chair Powell:”The Time has Come”

“The time has come,” the Chair announced,

“For easing to begin—

From tightening strings, and cautious holds—

And dovish, hawkish spin

And then the market breathed a sigh—

When at last the Fed gave in.”

Read:

Earth to Federal Reserve: What are you waiting for?

The Federal Reserve’s Analysis Paralysis

Andrew.Oliver@Compass.com

Earth to Federal Reserve: What are you waiting for?

This is the same headline I used in February 2022 in this article

Earth to Federal Reserve: What are you waiting for?,

when the Federal Reserve (Fed) was dithering about raising rates. It is just as applicable today as they dither about cutting rates.

Indeed, sometimes I wonder if the Fed is more concerned about coming up with catchy phrases: “transient inflation; “data dependent”; “higher for longer”; and now “data-dependent, not data point dependent” – than actually taking decisions.

“Date-dependent mean the Fed doesn’t have a clue”

This was a heading in an earlier Bloomberg article, which continued: But perhaps the bigger takeaway is that Chair Jerome Powell and his fellow policymakers really don’t have a clue what’s going to happen in the economy. They’re shooting in the dark. “They’re making it up as they go along.”

These comments may seem harsh but it expresses the frustration many feel about what I described in this recent article: The Federal Reserve’s Analysis Paralysis

The data is unreliable and subject to change

Mohamed El-Erian, whom I often quote, captured the current state of affairs when he observed: “I think the major issue is that the market has become overly data-dependent, just like our central banks have become overly data-dependent. So, we’re not looking beyond the next data release because we’re worried about what will the Fed do in September, what will the ECB (European) Central) Bank) do in September.”

Central bankers and markets should be aware of the risks associated with an overly data-dependent approach to monetary policymaking. In 2019, Powell himself highlighted the basic challenge: “We must sort out in real time, as best we can, what the profound changes underway in the economy mean for issues such as the functioning of labor markets, the pace of productivity growth, and the forces driving inflation.”

Yet economic data are often unreliable. Official statistics undergo multiple and often substantial revisions. For instance, the payroll numbers undergo subsequent revisions —sometimes large ones that give the lie to the initial perceptions.

Richard Fisher, a former Dallas Fed president, once offered an example of the dangers involved. Data pointing to excessively low levels of inflation had prompted the Fed to keep rates low in 2002 and 2003. Subsequent revisions, he acknowledged, showed that “inflation had actually been a half point higher than first thought. In retrospect, the real fed funds rate turned out to be lower than what was deemed appropriate at the time and was held lower longer that it should have been.”

In a recent Financial Times article, Mohammed-El Erian asked a number of questions, amongst them:

Why did Fed forecasts get it so wrong, be it on inflation or unemployment — the so-called dual mandate — in recent years? And to what extent has this resulted in a longer-term shift to excessive data dependency in the formulation of the central bank’s policy?

Ongoing structural and secular changes in how the US and global economies function are more consequential for policy design than “noisy” short-term data. So, is it not now time to combine data dependency with a much greater injection of forward-looking strategic thinking? (more…)

The Federal Reserve’s Analysis Paralysis

In November 2023, I wrote: “The question now is whether the Federal Reserve, having been extremely slow to start raising rates and reversing Quantitative Easing, will be similarly late in easing (rates). The Fed claims to be data dependent, but data tells us what happened in the past – and the Fed’s actions impact the future.”

The answer to that question is “yes” – and here we are, 8 months later, and the Fed is still “data dependent”, although this year’s mantra has become “higher for longer.”

(more…)

New Mortgage Applications Jump More Than 10%

WASHINGTON — Mortgage applications increased 10.4% from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending January 12, 2024. Last week’s results included an adjustment to account for the New Year’s holiday.

The Market Composite Index, a measure of mortgage loan application volume, increased 10.4% on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the index increased 26% compared with the previous week.

The Refinance Index increased 11% from the previous week and was 10% higher than the same week one year ago. The seasonally adjusted Purchase Index increased 9% from one week earlier. The unadjusted Purchase Index increased 28% compared with the previous week and was 20% lower than the same week one year ago.

“Mortgage rates declined across all loan types as Treasury yields moved lower last week on incoming inflation data, which helped to support a rise in mortgage applications. The 30-year fixed mortgage rate decreased six basis points to 6.75%, the lowest rate in three weeks,” said Joel Kan, MBA’s vice president and deputy chief economist.

“Compared to a holiday-adjusted week, both purchase and refinance applications were up, and the increases were heavily driven by the conventional market. Although purchase activity is lagging year-ago levels, refinance applications have improved from their recent low point and have been showing year-over-year gains, albeit at low levels. If rates continue to ease, MBA is cautiously optimistic that home purchases will pick up in the coming months.”

The survey covers over 75% of all U.S. retail residential mortgage applications and has been conducted weekly since 1990. Respondents include mortgage bankers, commercial banks, and thrifts. Base period and value for all indexes is March 16, 1990=100.

© 2024 Florida Realtors®

More Properties Listed, Supply Still Short

The recent pullback in mortgage rates is spurring more homeowners to put their homes up for sale, though the increases so far have been too modest to return the housing market’s inventory of available properties back to pre-pandemic levels.

The number of active listings, a tally of U.S. homes on the market that excludes those pending a finalized sale, climbed 4.9% to 714,176 in December from a year earlier, the biggest annual increase since June, according to data released this week by Realtor.com.

A big part of the increase was due to a 9.1% jump in new listings, or properties that made their market debut in December, which posted an annual increase for the second time after 17 months of declines.

As is typically the case, active listings declined in December from the previous month, falling 5.5%. But the drop was less than the typical decline of 6.8% to 13.2%, Realtor.com said.

While the pickup in home listings is a welcome development for prospective homebuyers, the housing market remains constrained with for-sale inventory still well below pre-pandemic levels.

Consider that active listings were down 30.9% in December compared to the same month in 2019, while new listings were down nearly 12%.

Housing economists expect that the average rate will continue to decline this year, though forecasts generally see it moving no lower than 6%.

That may not be enough to motivate many homeowners to sell, given that some two-thirds of U.S. homes have a mortgage with a rate under 4% and more than 90% have a rate below 6%.

That means the upcoming spring homebuying season is likely to favor sellers as homebuyers compete for a relatively limited number of homes for sale. (Florida Realtors)

And read these articles:

Why Mortgage Rates will fall in 2024

Transitory inflation? Recession? What else will forecasters get wrong?

More insurers coming to Florida

- Andrew Oliver, M.B.E., M.B.A.

Real Estate Advisor

Andrew.Oliver@Compass.com - AndrewOliverRealtor.com

m 617.834.8205

INFLATION and RECESSION UPDATE

This time last year, stocks were still in the gutter, inflation was in the stratosphere and Fed interest rates were going up, up, up. Today the S&P 500 has risen 17% since Jan. 1, the much-anticipated recession has yet to arrive, unemployment remains below 4% and consumers are still spending–Walmart, Target, and Gap all beat expectations this week.

Inflation has dropped to around 3%, not too far off the Fed’s 2% target. Walmart CEO Doug McMillon was talking about deflation in the coming months. Oil prices are below $75 a barrel, Airfares are significantly cheaper this year than they were for the holidays last year. Bond yields are dropping, too, as traders start to price in Fed rate cuts next year. The 10-year yield has dropped back to around 4.4% from as high as 5% in October. (Barrons)

On Thursday, Walmart CEO Doug McMillon said deflation could be coming as general merchandise and key grocery items, such as eggs, chicken and seafood get cheaper.

He said the retailer expects some of the stickier higher prices, such as the ones for pantry staples, to “start to deflate in the coming weeks and months,” too.

“In the U.S., we may be managing through a period of deflation in the months to come,” he said on the company’s Thursday earnings call. “And while that would put more unit pressure on us, we welcome it, because it’s better for our customers.”

“I think the most important observation we’ve made is that the worst of the inflationary environment is behind us,” Hone Depot, Chief Financial Officer Richard McPhail

The question now is whether the Federal Reserve, having been extremely slow to start raising rates and reversing Quantative Easing, will be similarly late in easing. The Fed claims to be data dependent, but data tells us what happened in the past – and the Fed’s actions impact the future.

“The Fed must lower rates to cause money suply to grow by 5% per year, consistent with the 2% inflation target.If the Fed waits until core inflation is 2% we could have a recession.”(Jeremy Siegel, Wharton)

And read these articles:

Why Mortgage Rates will fall in 2024

Transitory inflation? Recession? What else will forecasters get wrong?

More insurers coming to Florida

Core Inflation Prices Barely Budged in August

August Housing Market: Median Prices Rise Year on Year

Market Reports

BAY FOREST Q3 MARKET REPORT 2019-2023

BONITA BAY Q3 MARKET REPORT 2019-2023

IMPERIAL GOLF ESTATES Q3 MARKET REPORT 2019-2023 (more…)

Why Mortgage Rates will fall in 2024

This article addresses two things: what drives mortgage rates, and why they will fall.

What drives mortgage rates?

The Federal Reserve (Fed) meets regularly and announces, with great fanfare, its “Federal Funds Rate(FFR).” But what is this interest rate and what does it influence?

The FFR is the rate at which commercial banks borrow and lend their excess reserves to each other overnight. It is this rate which impacts the interest rate on many consumer loans, such as credit cards and automobile loans, but NOT 30-year Fixed-Rate Mortgages (FRM).

In general, FRM are sold to Fannie Mae and Freddie Mac and are bundled into portfolios which are sold to investors as Mortgage-Backed Securities (MBS). The yield investors demand for MBS is based upon the yield on the US Treasury 10-year (10T) yield, and the extra yield investors want to buy MBS rather than just risk-free Treasuries.

Look at this chart showing the three rates (FRM, FFR and 10T) over the last year. Note that the Green (FRM) and Red (10T) lines move in tandem, while the blue line (FFR) does not move with either of the other two. Thus, the FRM is determined by the yield on 10T, which is set by the market, and not by the Federal Reserve.

Transitory inflation? Recession? What else will forecasters get wrong?

Economists spent 2021 expecting inflation to prove “transitory.” They spent much of 2022 underestimating its staying power. And they spent early 2023 predicting that the Fed’s rate increases, meant to cure the inflation, would plunge the economy into a recession. (NY TIMES)

“US Economy Grew at a 4.9% Pace Last Quarter, Fastest Since 2021” (Bloomberg)

“The forecasts have been embarrassingly wrong, in the entire forecasting community. We are still trying to figure

out how this new economy works.” (Torsten Slok, Apollo Global Management)

“The economy is slowing faster than recent data suggests.” (Bill Ackman, Pershing Capital)

“I want to point out the central banks 18 months ago were 100% dead wrong. I would be quite cautious about what might happen next year.” (JPMorgan Chase CEO Jamie Dimon)

And read these articles:

More insurers coming to Florida

Core Inflation Prices Barely Budged in August

August Housing Market: Median Prices Rise Year on Year

Market Reports

BAY FOREST Q3 MARKET REPORT 2019-2023

BONITA BAY Q3 MARKET REPORT 2019-2023

IMPERIAL GOLF ESTATES Q3 MARKET REPORT 2019-2023 (more…)

Two More Ways the Mortgage Market differs from 2007/2008

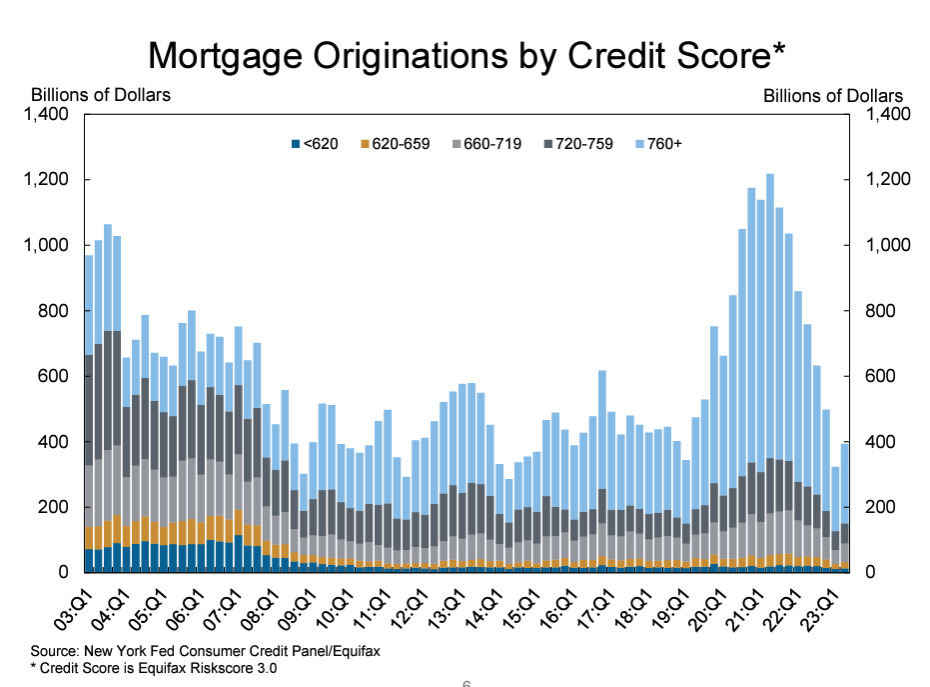

The chart below shows how loans with a credit score under 660 – the bottom colours of yellow and dark blue – which were about 20% of the total in the 2004-2007 period, have virtually ceased, with loans over 720 now making up the vast majority of new mortgages.

Two other changes:

Adjustable-rate mortgages can lead to higher default rates when interest rates rise, but they now represent less than 5% of total purchase and refinance loans, compared with over 35% at the peak of the pre-GFC (Global Financial Crisis) housing cycle. (FORTUNE)

The ratio of Americans’ mortgage debt to their real estate assets—also called loan-to-value—was just 27% in the second quarter, compared to over 40% in 2008 and roughly 50% in 2010. (Bank of America)

And read these articles:

More insurers coming to Florida

Core Inflation Prices Barely Budged in August

August Housing Market: Median Prices Rise Year on Year (more…)