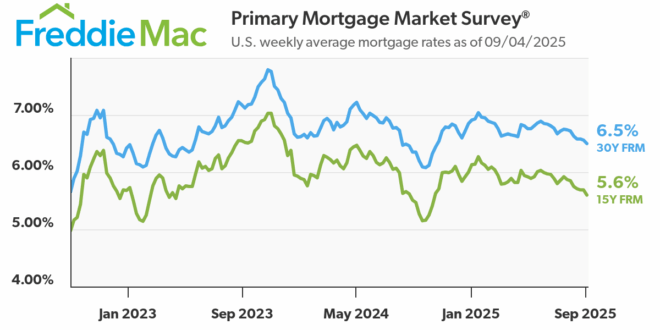

Are mortgage rates holding back the market?

I get asked this question regularly. The chart below covers the last 3 years, and shows that since September 2022 the 30-year FRM has been mostly between 6% and 7% with 3 spikes over 7%, and one drop to 6% in the fall of 2024.The current rate of 6.5% is in the middle of the range for most of the last 3 years.

How’s the Market in Naples in 2025?

This is, naturally, the most asked question by both buyers and sellers.

While there are always anecdotal stories – about both high- and low-priced sales – I try in this blog to focus on facts, actual sales data, albeit recognising that sales take place 4-8 weeks after a contract is signed. So sales are a lagging indicator; but they are neither selective nor influenced by emotion.

While I normally focus on quarterly numbers in less seasonal markets, here in Naples the market fluctuates so much with the calendar – more higher-priced take place during “the season” – that I report monthly figures.

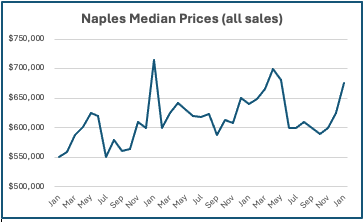

Here are the charts showing median prices since 2022 for all areas of Naples, broken down by property type. In broad terms the median price peaks each year in the early months, drifts lower in the summer months and recovers in the Fall. (more…)

How’s the market in February 2025?

This table shows median prices for all types of property sold in Naples month by month since 2020. There are a couple of outliers, but in general median prices have been in the $600-650,000 range. January 2025 was a little higher at $675,000.

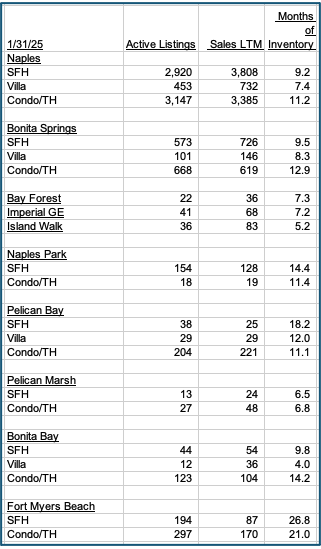

This table shows Active Listings divided by Sales in the last 12 months. The Months of Inventory number means how long it would take to sell the current inventory based upon the rate of sales in the previous year.Generally ,in real estate, 6 months of supply is regarded as a market in equilibrium between buyers and sellers: a higher number favours buyers, a lower number sellers.

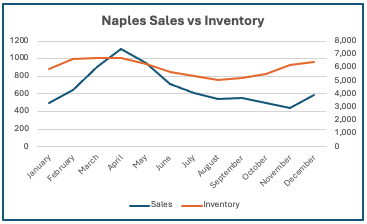

Southwest Florida is, of course, a seasonal market. The following chart shows that sales – which typically occur 6-8 weeks after a contract is signed – are at their highest in March-May, and lowest in October – January. Which makes sense. Inventory is highest in the early months, drops in the summer, and then picks up as we get towards the next season.

Comment

Anecdotal stories are intriguing, but often very selective. I try to present the actual numbers as a basis for making informed decisions by both sellers and buyers.

Andrew.Oliver@Compass.com

Fort Myers airport breaks passenger traffic record in 2024

“December 2024 was the busiest December in the 42-year history of the airport and we finished the year with a record-breaking 11,028,182 passengers, which was a 6.6% increase compared to the previous record set in 2022,” Steven Hennigan, executive director and CEO of the Lee County Port Authority, says in a statement.

The airline that saw the most traffic in December was Delta, with 212,801 passengers; it was followed by Southwest, with 171,903 passengers; United with 164,722 passengers; American with 147,042 passengers; and JetBlue with 110,179 passengers.

RSW had 10,362 aircraft operations (takeoffs and landings) in December, an increase of 5% compared with December 2023, according to a statement.

With more than 11 million passengers in 2024, RSW is one of the top 50 U.S. airports for passenger traffic. No ad valorem (property) taxes are used for airport operation or construction.(Business Observer)

Andrew.Oliver@Compass.com

Experts: Florida Insurance Market Solid

Despite warnings from two leading insurance rating agencies that Hurricane Milton weakened or threatened Florida’s troubled home insurance market, local experts say the market can manage losses from Milton and are ready to cover yet another hurricane, if one should come.

AM Best and Fitch Ratings each issued reports last week warning that Milton could stretch liquidity of Florida-based insurers that are primarily focused on protecting in-state homeowners.

But experts closer to Florida’s insurance industry cast doubt on AM Best’s and Fitch Ratings’ assertions. One reason is the two companies don’t rate most of the domestic Florida insurers whose financial strength they question, said Paul Handerhan, president of the Fort Lauderdale-based consumer-focused Federal Association for Insurance Reform.

“So AM Best and Fitch don’t have direct access to their reinsurance programs or financials,” Handerhan said. (more…)

Open Houses Sunday September 22: Bay Forest and Imperial Golf Estates

BAY FOREST

15535 CEDARWOOD LN, 5-304 (BERMUDA BAY 1)

2 Bed+DEN, 2 Bath

3rd (TOP) Fl, Impeccable

Updated KITCHEN/Baths

1538 SF, Garage

$460,000

Go HERE for photos and video

OPEN HOUSE SUNDAY 11:30-1:00

IMPERIAL GOLF ESTATES

1510 IMPERIAL GOLF COURSE BLVD #133 (THE ISLAND)

3rd (TOP) FL, Garage

2 Bed, 2 Bath

Dramatic Golf Course, Lake Views

Extra large rooms, 1538 Sq.Ft, Garage

$418,000

Open HOUSE SUNDAY 1:30-3:30 (will be listed in MLS on Monday with photos and video)

Recent Market Reports

Naples Mid-Year 2024 Market Report

Bonita Springs Mid-Year 2024 Market Report

Fort Myers Beach Mid-Year 2024 Market Report

Please contact me for a market report that includes properties in your area which were recently listed or sold.

Economic and mortgage commentary

The Federal Reserve’s new buzzword: Recalibrate

Federal Reserve Chair Powell:The Time has Come

Earth to Federal Reserve: What are you waiting for?”

The Federal Reserve’s Analysis Paralysis

Andrew.Oliver@Compass.com

Earth to Federal Reserve: What are you waiting for?

This is the same headline I used in February 2022 in this article

Earth to Federal Reserve: What are you waiting for?,

when the Federal Reserve (Fed) was dithering about raising rates. It is just as applicable today as they dither about cutting rates.

Indeed, sometimes I wonder if the Fed is more concerned about coming up with catchy phrases: “transient inflation; “data dependent”; “higher for longer”; and now “data-dependent, not data point dependent” – than actually taking decisions.

“Date-dependent mean the Fed doesn’t have a clue”

This was a heading in an earlier Bloomberg article, which continued: But perhaps the bigger takeaway is that Chair Jerome Powell and his fellow policymakers really don’t have a clue what’s going to happen in the economy. They’re shooting in the dark. “They’re making it up as they go along.”

These comments may seem harsh but it expresses the frustration many feel about what I described in this recent article: The Federal Reserve’s Analysis Paralysis

The data is unreliable and subject to change

Mohamed El-Erian, whom I often quote, captured the current state of affairs when he observed: “I think the major issue is that the market has become overly data-dependent, just like our central banks have become overly data-dependent. So, we’re not looking beyond the next data release because we’re worried about what will the Fed do in September, what will the ECB (European) Central) Bank) do in September.”

Central bankers and markets should be aware of the risks associated with an overly data-dependent approach to monetary policymaking. In 2019, Powell himself highlighted the basic challenge: “We must sort out in real time, as best we can, what the profound changes underway in the economy mean for issues such as the functioning of labor markets, the pace of productivity growth, and the forces driving inflation.”

Yet economic data are often unreliable. Official statistics undergo multiple and often substantial revisions. For instance, the payroll numbers undergo subsequent revisions —sometimes large ones that give the lie to the initial perceptions.

Richard Fisher, a former Dallas Fed president, once offered an example of the dangers involved. Data pointing to excessively low levels of inflation had prompted the Fed to keep rates low in 2002 and 2003. Subsequent revisions, he acknowledged, showed that “inflation had actually been a half point higher than first thought. In retrospect, the real fed funds rate turned out to be lower than what was deemed appropriate at the time and was held lower longer that it should have been.”

In a recent Financial Times article, Mohammed-El Erian asked a number of questions, amongst them:

Why did Fed forecasts get it so wrong, be it on inflation or unemployment — the so-called dual mandate — in recent years? And to what extent has this resulted in a longer-term shift to excessive data dependency in the formulation of the central bank’s policy?

Ongoing structural and secular changes in how the US and global economies function are more consequential for policy design than “noisy” short-term data. So, is it not now time to combine data dependency with a much greater injection of forward-looking strategic thinking? (more…)

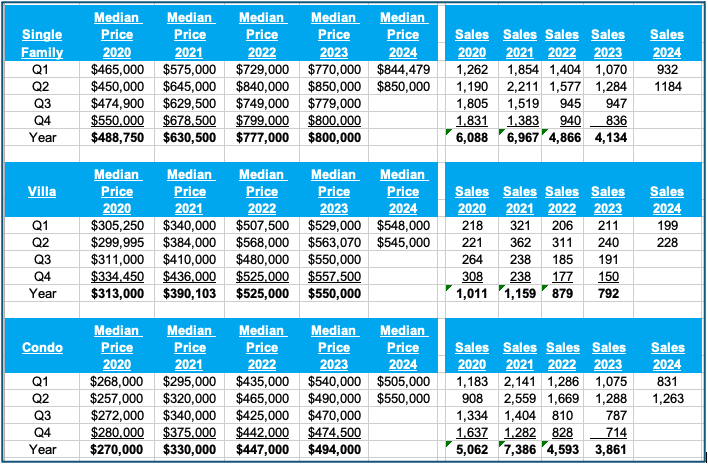

Naples Mid-Year 2024 Market Review

Despite some media reports suggesting a decline in Naples’ property prices, the data on completed sales supports my view that the market remains stable in overall terms as far as prices, while sales have returned to pre-COVID levels. This table shows Median Prices and Sales for Single Family, Villa and Condos

The median Price per Sq.Ft. increased for SFs in line with median prices, and was stable for Villa and Condos.

DTO – Days To Offer – the number of days a property is listed before an accepted offer is received – increased, but was still below 2020 speeds. (more…)

Another Bay Forest Sale

To see how I present a property to the market Go HERE to see the photos and videos of the above property.

And Go HERE to see details of the one that is still available in La Jolla. (more…)

It’s been an active week in Bay Forest!

2 more properties have gone under contract this week and 2 sales have closed, as work continues on the new boardwalk.

Go HERE to read the latest progress report. (more…)

Exciting News from Bay Forest – and Open House TODAY 12-4

“WE ARE EXCITED TO ANNOUNCE THE BUILDING PERMIT TO START CONSTRUCTION ON THE BOARDWALK WAS ISSUED TODAY. URS WILL BE ONSITE MONDAY, MAY 20TH AND WORK WILL RESUME.”

There are 10 properties currently Under Contract in Bay Forest, supporting my argument that this is a great time to buy, especially now that construction of the new $4.5 million Boardwalk is about to resume. (more…)

Assessments and Reserves

Costs

Every home on the planet needs maintenance, repairs, upgrades, renovations and improvements over time. No property is immune from this. Every homeowner knows that when a roof needs to be repaired, it’s wisest not to delay….. keeping a reserve fund for these inevitable costs is essential, whether a single family home or an apartment building.

Options

Owners of homes have two options as it relates to funding bigger cost items: either you build up a ‘savings account’ of sorts by adding a bit extra each month into the kitty to create a reserve fund, or you keep in the back of your mind the knowledge and certainty that at some point you will have to fund a bigger expenditure another way. In condo’s and co-ops that is done via an assessment….eg: A $1 million facade repair is split amongst 100 apartment owners so that each pays a percentage of that cost based on the percentage of the building they ‘own’ based on their offering plan or number of shares.

Financing (more…)

8 new Property Insurance Companies approved to enter Florida market

Following historic legislative reforms designed to promote market stability, eight property and casualty insurers were approved to enter Florida’s insurance market. Ovation Home Insurance Exchange, the most recent approval, joins Manatee Insurance Exchange, Condo Owners Reciprocal Exchange, Orange Insurance Exchange, Orion180 Select Insurance Company, Orion180 Insurance Company, Mainsail Insurance Company, and Tailrow Insurance Companies as newly approved property and casualty insurers.

“Florida’s insurance market continues to strengthen, showing signs recent legislation is having positive impacts to the property insurance market,” said Insurance Commissioner Michael Yaworsky. “OIR remains steadfast in our efforts to stabilize Florida’s insurance market by implementing legislative reforms and recruiting more insurers to the state. We look forward to continuing this work and promoting a competitive market for policyholders.”

In addition to new companies entering the market, OIR approved the acquisition of Florida domestic property and casualty reciprocal insurer, Trusted Resource Underwriters Exchange, to allow the existing company to grow its footprint in the state and expand its underwriting capacity. As a result of OIR’s approval of the acquisition, more than $1.25 billion of capital is being invested into Florida’s property and casualty insurance market.

Citizens Property Insurance Corporation

Citizens Property Insurance Corporation (Citizens) is showing improvement in their financial strength over the previous years. For instance, Citizens’ surplus increased by approximately 17.5 percent from previous years and Citizens posted a net income in 2023 of $746 million compared to a loss of $2.2 billion in 2022. Additionally, Citizens’ combined ratio improved from the previous year from 204.4 percent to 59.5 percent.

As the market continues to stabilize, OIR is seeing a continued interest from authorized insurers in the Citizens Depopulation program. In 2024, OIR has approved 13 companies to assume more than 354,000 policies from Citizens. In 2023, more than 275,000 policies were assumed from Citizens, reducing Citizen’s exposure by more than $113 billion.

Florida Domestic Company Strength (more…)

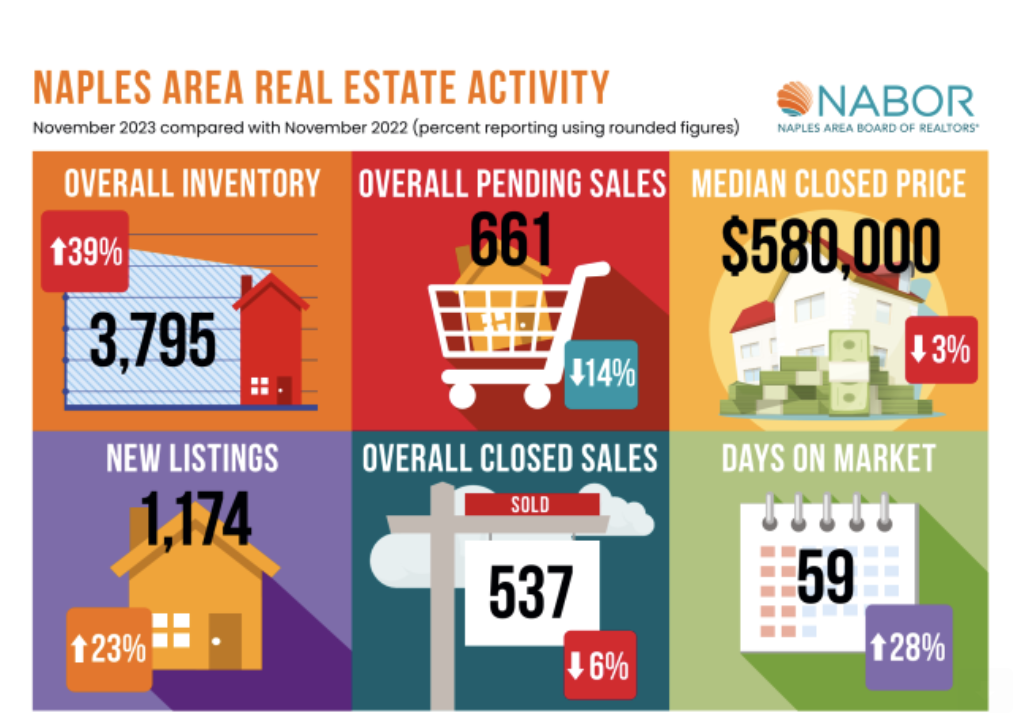

Naples November Market Highlights

My year end reviews will be published on January 14.

And read these articles:

INFLATION and RECESSION UPDATE

Why Mortgage Rates will fall in 2024

Transitory inflation? Recession? What else will forecasters get wrong?

More insurers coming to Florida

Core Inflation Prices Barely Budged in August

August Housing Market: Median Prices Rise Year on Year

Market Reports

BAY FOREST Q3 MARKET REPORT 2019-2023

BONITA BAY Q3 MARKET REPORT 2019-2023

IMPERIAL GOLF ESTATES Q3 MARKET REPORT 2019-2023 (more…)

More insurers coming to Florida

More insurance companies have come to do business in Florida, according to State Representative Bob Rommel.

Rommel said that the four carriers coming will not officially sell you a policy until hurricane season is over. There are three more insurers that are in the process of coming into the state as well.

“Before we got the bill, there was a fear that there will be little or no reinsurance money available for insurance carriers, which they need. Since we passed the bill, everybody has been able to get reinsurance, so I think that there is a light at the end of the tunnel,” said Rommel.

According to Rommel, he’ll continue addressing the state’s insurance crisis when legislators meet again in 2024 (WINKNews) (more…)