Core Inflation Prices Barely Budged in August

While inflation rose 3.5% year-to-year in Aug. – still above the Fed’s 2% goal – it was only up 0.1% month-to-month after backing out higher gas prices.

Core inflation slows

But excluding the volatile food and gas categories, “core” inflation rose by the smallest amount in almost two years in August, evidence that it’s continuing to cool. Fed officials pay particular attention to core prices, which are considered a better gauge of where inflation might be headed.

Core prices rose just 0.1% from July to August, down from July’s 0.2%. It was the smallest monthly increase since November 2021.

Compared with a year ago, (more…)

Credit Score Change Could Help Millions of Buyers

The nation’s consumer bureau took a first step to erase medical debt from credit reports and lending decisions because that type of debt “has little predictive value.”

The Consumer Financial Protection Bureau (CFPB) outlined proposals under consideration – moves that it says would help families recover from medical crises, stop debt collectors from coercing people into paying bills they may not owe, and ensure that creditors don’t rely on data that is often plagued with inaccuracies and mistakes.

“Research shows that medical bills have little predictive value in credit decisions, yet tens of millions of American households are dealing with medical debt on their credit reports,” says CFPB Director Rohit Chopra. “When someone gets sick, they should be able to focus on getting better rather than fighting debt collectors trying to extort them into paying bills they may not even owe.”

“Access to health care should be a right and not a privilege,” Vice President Kamala Harris told reporters as she helped CFPB make the announcement. “These measures will improve the credit scores of millions of Americans so that they will better be able to invest in their future.” (more…)

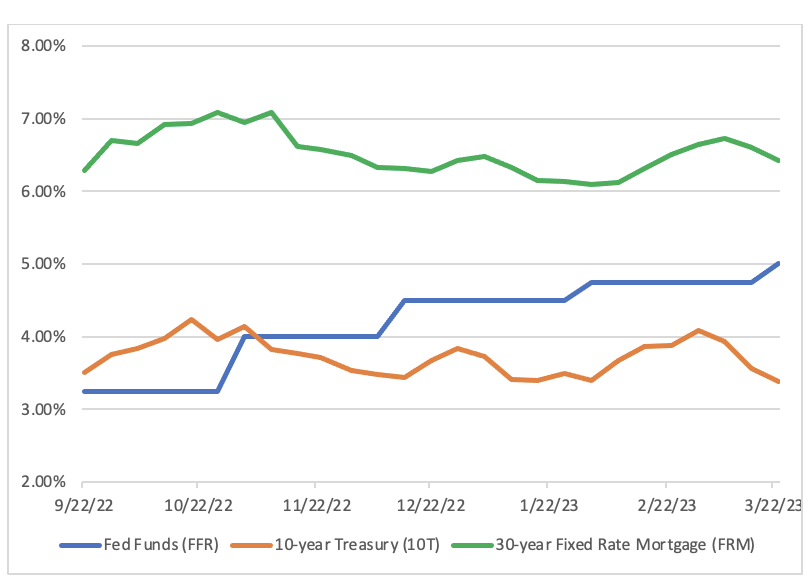

Federal Reserve increase rates; Mortgage Rates drop

Too often I see a headline like this one: “Mortgage Rates Continue to Slide Despite Fed Hike.” The 30-year Fixed Rate Mortgage (FRM) does NOT follow the Federal Reserve’s rate increases!

Look at this chart for the last few months:

Note the correlation between the 10T (red line) and FRM (green) – and the lack of correlation between FFR (blue) and FRM.

Let’s look at this another way, the spread (difference) between the FRM and 10T, and between FRM and FFR:

Over the last 6 months, the spread between FRM and 10T has been in a tight band between 2.69% and 3.04%, while that between FRM and FFR has dropped from 3.04% to 1.42%.

For a more detailed explanation of what drives mortgage rates – and why the FRM will fall at some point – read Why Mortgage Rates Will Fall

And read these articles:

What drives Mortgage Rates in one chart

Lies, Damned Lies and Inflation “Statistics”*

HOW AND WHEN WILL HOUSING REBOUND? (more…)

Florida lawmakers eye property insurance reforms

Over the past year, state lawmakers have made changes on paper through several attempts to cure Florida’s property insurance crisis. But a homeowner in Florida who opens their annual renewal and sees their premium has increased, or finds out their carrier has suddenly dropped them, may not have noticed anything different.

State Sen. Jim Boyd, R-Bradenton, noted during the first of last year’s special sessions to address insurance that relief from any measures taken by lawmakers wouldn’t be realized for at least another 18 months. That session took place in May 2022.

Since then, two hurricanes hit the state. Lawmakers then held a second special session on insurance in December. Six property insurance companies were declared insolvent last year. Citizens Property Insurance Corp., the state-run “insurer of last resort,” continues to grow with more than 1 million policies.

And now the annual, 60-day regular legislative session is underway. The session is largely where party-line battles are taking center stage, but not insurance. And those homeowners with delayed or unfulfilled property damage claims may find their legal recourses slashed, owing to legislation approved in the special sessions to limit what the insurance industry and lawmakers said was too much litigation over property insurance claims and disputes between homeowners and their insurers.

The story remains the same as it was a year ago: it’s lawyers, contractors and public adjusters versus lawmakers and insurance companies. (more…)

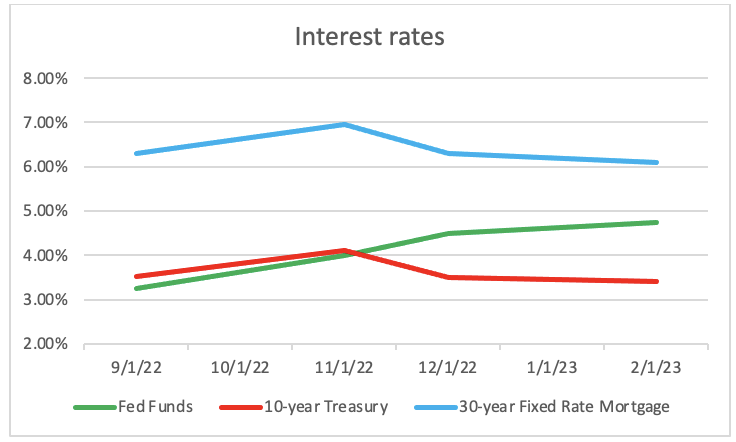

What drives Mortgage Rates in one chart

I can explain as often as I do that the 30-year Fixed rate Mortgage (FRM) is based upon the yield on the US 10-year Treasury (10T), not the Federal Reserve’s Fed Funds rate (FFR), but still I read regularly comments such as “mortgage rates will move up after the Fed increased its interest rate.”

Look at this chart for the last few months, the dates being those when the Federal Reserve increased its interest rate:

Note the correlation between the 10T (red line) and FRM (blue) – and the lack of correlation between FFR and FRM.

Let’s look at this another way, the spread (difference) between the FRM and 10T and between FRM and FFR:

Over the last 5 months, the spread between FRM and 10T has been in a tight band between 2.69% and 2.85%, while that between FRM and FFR has dropped by a huge 1.7%.

For a more detailed explanation of what drives mortgage rates – and why the FRM will fall at some point – read Why Mortgage Rates Will Fall

And read these recent articles: (more…)

Lies, Damned Lies and Inflation “Statistics”*

My daughter, who works for the Bank of England, is studying for her Master’s in Economics at the University of Edinburgh, and sent me one of her papers. It was filled with a vast array of complex mathematical equations of which I could make no sense, despite being a mathematician by training and studying Economics at Oxford…..a few years ago.

The Federal Reserve has teams of economists plus input from Reserve Banks all around the country. The Bureau of Labor Statistics, which produces the Consumer Price Index (CPI), has another battalion of experts. All this talent must, one could fairly assume, produce sophisticated and accurate models for inflation.

Imagine my surprise, therefore, to discover that one key element, housing inflation – which constitutes one-third of the CPI and 40% of “core” inflation (excluding food and energy) – is an imputed number (“assigned by inference”), not an actual one.

Read what Nobel prize-winning Economist Paul Krugman wrote recently: ”How does the bureau measure housing inflation? Not by looking at the prices at which houses are sold, which fluctuate a lot with things like interest rates. Instead, it looks at how much renters pay — and for the large number of Americans who own their own homes, it imputes what it calls Owners’ Equivalent Rent, an estimate based on rental markets of what homeowners would be paying if they were renters (or, if you like, the rent they are implicitly paying to themselves).

The trouble is that this measure relies on average rents, which to a large extent reflect leases signed many months ago. A new Fed study shows that official rent measures lag market rents by about a year. And here’s the thing: Market rental rates exploded in 2021, probably as a result of the rise in working from home, but have since leveled off and may in fact be falling.

So official inflation measures are telling us about what was happening a year ago; they overstate current inflation and, perhaps more important, grossly understate the extent to which the inflation picture has improved. If you try to measure inflation excluding those dubious housing numbers, plus other volatile elements, you get a picture of dramatic improvement, almost enough to declare the inflation surge over.”

Let’s look at inflation.There are more gauges of inflation than the UK had Prime Ministers in 2022, but let’s just look at Personal Consumption Expenditures (PCE is the value of the goods and services purchased by, or on the behalf of, “persons” who reside in the United States.). (more…)

Why Mortgage Rates Will Fall

I have read and heard several comments suggesting that the increase in the 30-year Fixed Rate Mortgage (FRM) this year has been a direct result of the increase in the Federal Reserve’s Fed Funds rate (FF).

This is not correct.

As I will demonstrate, the FRM is determined by market forces, and in particular by the extra yield – the “spread” – which investors require when buying pools of mortgages (Mortgage Backed Securities or MBS), as compared with the risk-free yield available with the 10-year Treasury Note (10T) which has the nearest duration to the expected life of a pool of mortgages.

In contrast, the FF is the rate that banks use when setting their Prime Rates. When the FF increases, banks increase their Prime Rates and therefore the interest rate on those loans whose rates are based upon Prime Rates – e.g. credit cards and auto loans.

And we will see that the FRM increased this year long before the Fed started to increase the FF rate.

Mortgage-Backed Securities (MBS)

A conventional mortgage or conventional loan is any type of home buyer’s loan that is not offered or secured by a government entity. Instead, conventional mortgages are available through private lenders, such as banks, credit unions, and mortgage companies.

Most conventional mortgages are packaged into mortgage-backed securities and sold to investors. This allows the bank or originator to use its capital to finance more mortgages.

The relationship between 10T and FRM

This chart shows how the two have moved in lockstep over the last 30-plus years:

Source: National Association of Realtors

While the “spread” has mostly been in the 1.5-2% range, it has fluctuated, especially during times of financial stress or uncertainty: (more…)

Mortgage Rates peaked? I spoke too soon

In June I published Have Mortgage Rates peaked? when the 30-year national average Fixed-Rate Mortgage (FRM) reached 5.81% and commented: “..a realistic expectation would be that the spread (the difference between the FRM and the yield on the 10-year Treasury) will drop from its current 2.5% to at least 1.8% at some point. If the yield on 10T stays in the low 3% range that would suggest that the FRM will drop below 5% again.”

Well it did…for a while, dropping to 4.99% on August 4th.

But then this happened:

Why have mortgage rates jumped again? (more…)

Is the U.S. Housing Market at a Crossroads?

Homes reached record prices in early 2022 – so is the current market a housing recession or just a market correction?

Here are some extracts from an article Market at the Crossroads on the Florida Realtors website, with my comments and links to recent articles at the end.

Is there a housing slowdown?

There is widespread consensus that the housing market has experienced a drastic drop-off in activity since its pandemic-prompted heights.

The housing market is “not like the volatile stock market, always going up and down; the housing market moves at a different, slower pace. “The market simply could not, and was never expected to, grow at that pace indefinitely,” Neda Navab, president of brokerage operations at real estate company Compass said. “Whether this trend will continue long enough for the market to enter a true ‘recession,’ or if this is simply the start of an expected ‘correction’ to historic norms, still remains to be seen.”

The case for a housing correction (more…)

Recession: what Recession?

The August jobs report published yesterday showed that the labour market remained red-hot in July despite expectations job growth would cool as tighter monetary conditions and company layoffs stoked fears of a recession.

Here were the key numbers from the report, compared to economist estimates compiled by Bloomberg:

Non-farm payrolls: +528,000 vs. +250,000 (more…)

No, the Federal Reserve does not control mortgage rates

There is widespread misunderstanding about what drives mortgage rates. Indeed, I read an article recenlty on the National Association of Realtors website which stated that mortgage rates had risen sharply following the increase in the Federal Reserve’s interest rate.

Not so. (more…)

Recession? Yes, no, maybe……..

When I proposed to my wife, she was taken by surprise and responded: “Yes, no, maybe.”

I was reminded of that response while listening to all the conversations in recent days about whether or not the US already in, is about to be in, or will escape a recession.

A lot of the confusion relates to the question: “how do you define recession?” and “who gets to decide if it is a recession?”

And no, it’s not by Punxsutawney Phil looking for his shadow.

What is a recession? (more…)

Federal Reserve tries to rewrite history

Two comments from Federal Reserve Chair Powell struck me while I was listening to his Press Conference on Wednesday:

On the “speed” of the Fed’s move to increase rates:

“When inflation changed direction, really, in October. We’ve moved quickly since then. I think people would agree. But before then, inflation was coming down month by month. And we kind of thought we had the story. Probably had the story right. But then I think in October, you started to see a range of data that said no. This is a much stronger economy and much higher inflation than we’ve been thinking.”

Moved quickly? (more…)

Has Inflation Peaked?

After I published Have Mortgage Rates peaked? last week a reader asked me why I thought the yield on the 10-year Treasury Bill would not continue to increase, so that even if the spread over the 30-year Fixed Rate Mortgage (FRM) narrowed, the FRM rate itself might still increase.

In Are we already in a Recession?, published on June 18, I wrote: “Just as the yield on 10T has more than doubled since pre-COVID while the Fed Funds rate is unchanged, so the Fed Funds rate can increase sharply – the Fed is forecasting it will reach 3.4% this year, also double its pre-COVID level – without necessarily impacting the yield on 10T. That will depend upon the economic outlook. Ironically, perhaps, the more determined the Fed is to drive down inflation – even at the cost of a recession and higher unemployment – the greater the chance that the yield on 10T – and by extension the FRM – will decline – at some point.”

In the last few days, as more economists talked about a recession after the Atlantic Fed updated its Q2 GDP estimate to minus 2.1% (it was 0% when I wrote on June 18), the yield on 10T has dropped sharply, falling to 2.9% from a peak of 3.5% in the middle of May: (more…)

Have Mortgage Rates peaked?

With all the noise about the determination of the Federal Reserve (Fed) to continue to increase interest rates it might be tempting to asume that mortgage rates will continue to rise.

But I believe there are good reasons for thinking that mortgage rates may have peaked. Read on to find out why I think this.

Current rates

The 30-year Fixed rate Mortgage (FRM) reached its highest level since 2008 this week: (more…)