Why Mortgage Rates will fall in 2024

This article addresses two things: what drives mortgage rates, and why they will fall.

What drives mortgage rates?

The Federal Reserve (Fed) meets regularly and announces, with great fanfare, its “Federal Funds Rate(FFR).” But what is this interest rate and what does it influence?

The FFR is the rate at which commercial banks borrow and lend their excess reserves to each other overnight. It is this rate which impacts the interest rate on many consumer loans, such as credit cards and automobile loans, but NOT 30-year Fixed-Rate Mortgages (FRM).

In general, FRM are sold to Fannie Mae and Freddie Mac and are bundled into portfolios which are sold to investors as Mortgage-Backed Securities (MBS). The yield investors demand for MBS is based upon the yield on the US Treasury 10-year (10T) yield, and the extra yield investors want to buy MBS rather than just risk-free Treasuries.

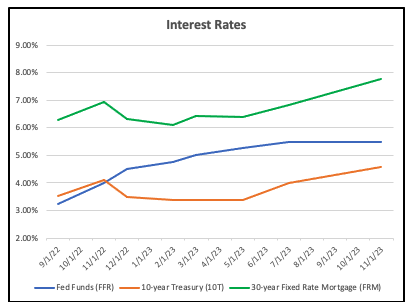

Look at this chart showing the three rates (FRM, FFR and 10T) over the last year. Note that the Green (FRM) and Red (10T) lines move in tandem, while the blue line (FFR) does not move with either of the other two. Thus, the FRM is determined by the yield on 10T, which is set by the market, and not by the Federal Reserve.

The Spread

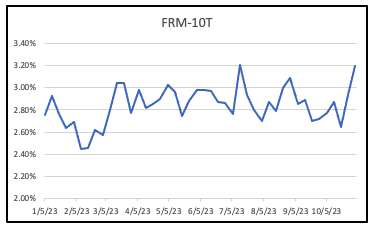

The spread – reflecting the extra yield investors want to buy MBS – between FRM and 10T this year has between 2.5% and 3.2%. That is unusually high, as we shall see.

Why Mortgage rates will Fall

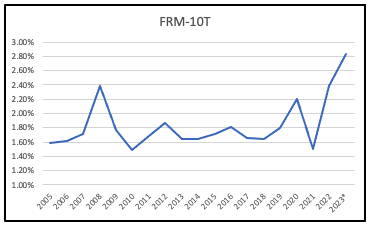

And now to the forecast. The spread between FRM and 10T is much higher than it is in “normal” times. Look at this chart going back to 2005:

For most of the last 18 years the spread has been in the 1.6 – 1.8% range and has average around 1.75%. The exceptions have been:

2008 – the Great Recession and the height of the foreclosure crisis making mortgages unattractive to investors, who demanded higher yields

2020 – at the outset of the pandemic, amidst widespread uncertainty, spreads widened before the Fed started its huge program of pouring money into the economy, buying both Treasuries and MBS and igniting an asset boom

2022-23 – when the Fed finally, belatedly, stopped injecting liquidity into the system, the market reacted to two main factors: the Treasury would need to sell a lot more Securities to fund the spending, and the growing Budget deficit; and the biggest buyer of Treasuries – the Fed itself – was switching from being a buyer to a seller.

This resulted in the most basic economic equation – more sellers than buyers, so the price of Treasuries went down and the yield (which moves inversely to the price) went up.

How far will mortgage rates fall?

Few if any forecasts have been accurate over the last few years, so it would be foolish for me to suggest a timeframe.

What is less foolish is to suggest that the era of cheap money over the last 15 years has ended. It is only in that period that the yield on 10T has been below 4%, and a sustained return to a 4% yield on 10T is likely.

That in turn would suggest a sub 6% FRM.

Not 3%, but better than 7.7%.

And read these articles:

Transitory inflation? Recession? What else will forecasters get wrong?

More insurers coming to Florida

Core Inflation Prices Barely Budged in August

August Housing Market: Median Prices Rise Year on Year

Market Reports

BAY FOREST Q3 MARKET REPORT 2019-2023

BONITA BAY Q3 MARKET REPORT 2019-2023

IMPERIAL GOLF ESTATES Q3 MARKET REPORT 2019-2023

Home Prices Are Rebounding

Insurance Reform : Premiums still rising sharply

How to protect your house from title fraud

Florida lawmakers eye property insurance reforms

Expansion Plans for Fort Myers Airport

Guide to Buying and Selling in Southwest Florida

Mortgage and Economic commentary

Why Mortgage rates Will Fall

What drives Mortgage Rates in one chart

Lies, Damned Lies and Inflation “Statistics”*

- Andrew Oliver, M.B.E., M.B.A.

Real Estate Advisor

Andrew.Oliver@Compass.com - AndrewOliverRealtor.com

m 617.834.8205