BONITA BAY MARKET 2024 MARKET REPORT and 5-YEAR REVIEW

Median Price and Sales

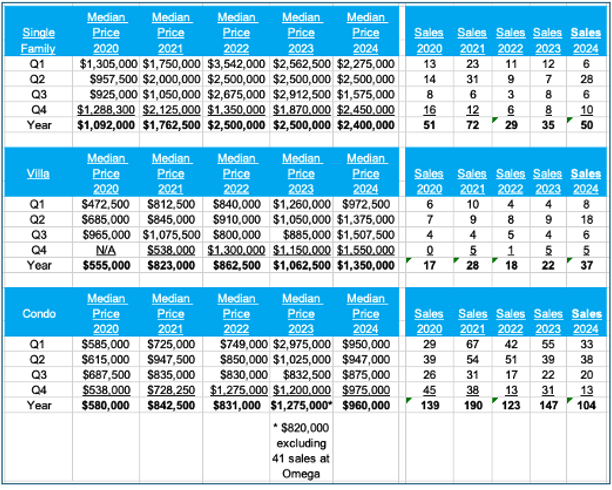

The median price of the Single Family homes sold in Bonita Bay more doubled from $1.1 million in 2020 to $2.5 million in 2022 and has been stable since.

Sales increased from 2019 to 2021, dropped back, and them increased in 2024.

The median price of the Villas sold in Bonita Bay has continued to increase year by year, and sales also increased last year,

The median price of the Condos sold in Bonita Bay has also continued to increase. On the surface, the median price jumped to $1.275 million in 2023, but the 41 sales at Omega boosted the median price. Without those sales, the 2023 median price would have been $820,000, meaning there was an underlying increase again in 2024. Excluding the Omega sales in 2023, the 2024 figure was steady.

While Inventory has doubled from the extremely low levels on 2022/23, it has returned to more normal levels at the beginning of the season.

Price per Sq Ft (PSF) and Speed of Sales (Days to Offer Accepted – DTO)

PSF is another way to look at prices.

The PSF has increased significantly in recent years, in line with median prices.

The pace of Sales quickened dramatically until 2022. 2024 presented mixed picture. (more…)

PELICAN BAY MARKET 2024 MARKET REPORT and 5-YEAR REVIEW

Median Price and Sales

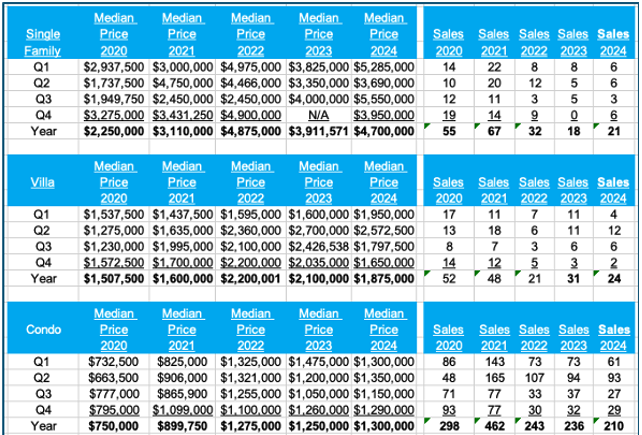

The median price of the Single Family homes sold in Pelican Bay more doubled from $2.25 million in 2020 to $4.7 million in 2024.

Sales increased until 2021 and have since dropped back below pre-pandemic levels.

The median price of the Villas sold in Pelican Bay increased from $1.5 million in 2020 to $1.875 million in 2024, but declined from 2022/23 levels.

The number of sales increased in 2020/21, but has since dropped back to pre-pandemic numbers.

The median price of the Condos sold in Pelican Bay increased 45% from $750,000 in 2020 to $1.3 million in 2024, and was stable from 2022-24. Sales have also dropped sharply since 2021.

Price per Sq Ft (PSF) and Speed of Sales (Days to Offer Accepted – DTO)

PSF is another way to look at sales. (more…)

BONITA SPRINGS 2024 MARKET REPORT and 5-YEAR REVIEW

Median Price and Sales

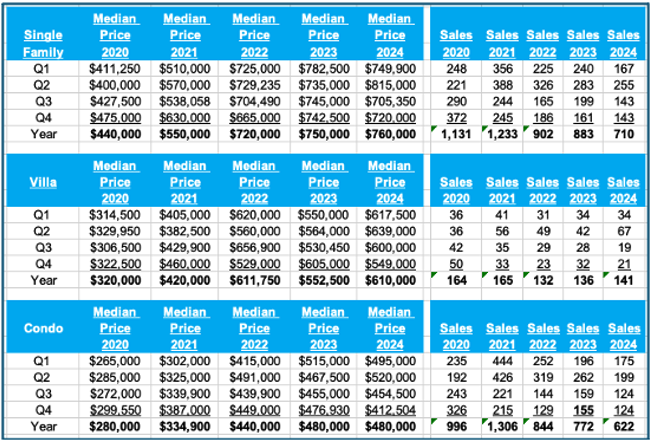

The median price of the properties sold in Bonita Springs increased dramatically during the cheap money period after COVID. Single Family and Condo median prices increased almost 60% from 2020 to 2022, while Villa median prices increased by 90%.

Prices have been more stable in the last 2 years. There are always quarterly fluctuations in real estate sales and median prices. In Southwest Florida that can be exacerbated by the seasonal nature of the market. Many of the more expensive properties are bought by people wintering here and thus – except during the post COVID rush – median prices are often strongest during the winter months.

If prices fall during the second half of a year, it is hard to tell whether that decline reflects just the lower price of the properties that did sell, or a reduction in actual prices. What can be said in early 2025 is that attorneys report a pick-up in activity after the Election, which removed an uncertainty, and agents are reporting that Open Houses in early January have been very busy.

Overall sales – of all property types – surged until around Q3 2021, and then almost halved from 2021 to 2024, when they were at the lowest since 2009.

(more…)

(more…)

NAPLES 2024 MARKET REPORT and 5-YEAR REVIEW

Median Price and Sales

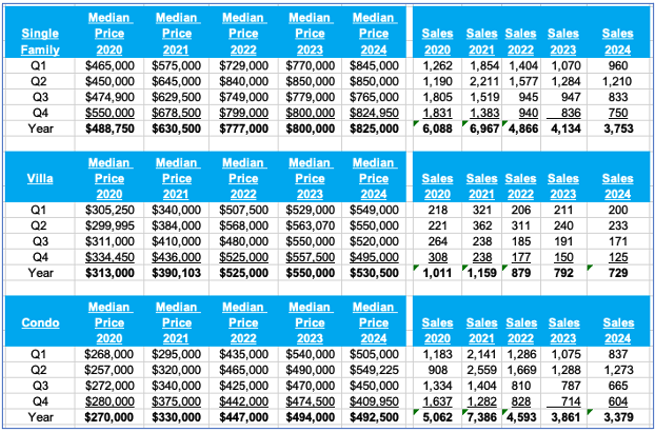

The median price of the properties sold in Naples increased dramatically during the cheap money period after COVID. Single Family median prices increased almost 60% from 2020 to 2022; Villa and Condo median prices by two-thirds.

Prices have been more stable in the last 2 years. There are always quarterly fluctuations in real estate sales and median prices. In Naples that can be exacerbated by the seasonal nature of the market. Many of the more expensive properties are bought by people wintering in Naples and thus – except during the post COVID rush – median prices are often strongest during the winter months.

If prices fall during the second half of a year, it is hard to tell whether that decline reflects just the lower price of the properties that did sell, or a reduction in actual prices. What can be said in early 2025 is that attorneys report a pick-up in activity after the Election, which removed an uncertainty, and agents are reporting that Open Houses in early January have been very busy.

Overall sales – of all property types – surged until around Q3 2021, and then halved from 2021 to 2024, when they were at the lowest since 2010.

(more…)

(more…)

Naples Housing Market Surges in January 2025

The Naples real estate market kicked off 2025 with strong momentum, as buyers and sellers saw new opportunities amid rising inventory and stable price trends. According to the latest report from the Naples Area Board of REALTORS® (NABOR®), closed sales in January increased by 12%, with 551 homes sold compared to 492 in January 2024.

The median closed price rose 9.4% year-over-year, reaching $659,000, signaling continued demand for homes in the area. However, while appreciation has slowed from the rapid increases seen in 2021 and 2022, the market remains dynamic, with price fluctuations depending on property type and location.

Inventory Expands, Giving Buyers More Choices (more…)

Bay Forest, Imperial, PRICE REDUCTIONS and OPEN HOUSES

The Bay Forest Boardwalk is finished and just waiting on permits to open offically. Several properties have reduced prices this weekend so now is a GREAT time to buy!

SATURDAY OPEN HOUSES

THE ISLAND, IMPERIAL GOLF ESTATES

10 AM – 12 PM

1510 IMPERIAL GC BLVD, 133

2 Bed, 2 Bath

3rd (TOP) Fl, Garage

Dramatic Golf Course, Lake Views; 1538 Sq.Ft,

LARGE ROOMS, FEELS LIKE SINGLE FAMILY LAYOUT

$399,000 now $380,00

GO HERE for photos, video, floor plan, etc

BAY FOREST OPEN HOUSE SATURDAY 1-3 PM

LAKESIDE VILLA IN RARELY AVAILABLE LA JOLLA

15455 ROYAL FERN LN N, #37A

2 Bed+DEN, 2 Bath

GARAGE

$533,000 now $505,000

Go HERE for photos, video etc

SUNDAY OPEN HOUSES

BAY FOREST

OPEN HOUSE 12:30-2:30 PM

SANDY PINES

15450 CEDARWOOD LN #203

STUNNING LAKE VIEW

COMPLETELY UPDATED

2 bed 2 Bath; Garage

$525,000 now $499,000

Go HERE for photos and more

OPEN HOUSE 2-4 PM

15348 WIMBORNE LN

Rarely available Sea Pines I single-family home . FLEXIBLE floor plan allows for two or three bedrooms, plus a family room and office, DOUBLE GARAGE and 34ft LANAI

$640,000 now $600,000

Go (a href=”https://tour.realtoursswfl.com/sites/15348-wimborne-ln-naples-fl-34110-13212150/branded”<HERE for photos and more

OPEN HOUSE SUNDAY 2:45-4:45 PM

BERMUDA BAY 1

15435 CEDARWOOD LN, 5-304

2 Bed+DEN, 2 Bath

3rd (TOP) Fl, Impeccable

NEW A/C, NEW Ductwork

Updated KITCHEN/Baths

Garage, $460,000

Go HEREfor photos, videos and more

Andrew.Oliver@Compass.com

How’s the market in February 2025?

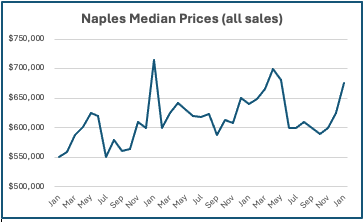

This table shows median prices for all types of property sold in Naples month by month since 2020. There are a couple of outliers, but in general median prices have been in the $600-650,000 range. January 2025 was a little higher at $675,000.

This table shows Active Listings divided by Sales in the last 12 months. The Months of Inventory number means how long it would take to sell the current inventory based upon the rate of sales in the previous year.Generally ,in real estate, 6 months of supply is regarded as a market in equilibrium between buyers and sellers: a higher number favours buyers, a lower number sellers.

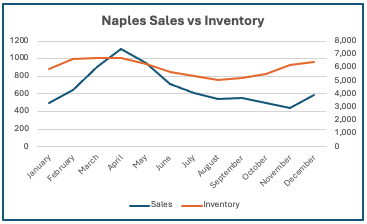

Southwest Florida is, of course, a seasonal market. The following chart shows that sales – which typically occur 6-8 weeks after a contract is signed – are at their highest in March-May, and lowest in October – January. Which makes sense. Inventory is highest in the early months, drops in the summer, and then picks up as we get towards the next season.

Comment

Anecdotal stories are intriguing, but often very selective. I try to present the actual numbers as a basis for making informed decisions by both sellers and buyers.

Andrew.Oliver@Compass.com

Bay Forest Open House TODAY 1-3 PM

This stunning 2nd-floor condo with cathedral ceilings offers a blend of luxury, modern updates, and tranquility, and comes fully furnished.Go HERE for more photos, video, and more.

Come to today’s Open Houses 1-3 PM or call Andrew Oliver:617.834.8205 for a private showing

As you step inside, you’ll be captivated by the breathtaking view through the lanai overlooking the lake, elegant wood laminate flooring and soaring ceilings.

The updated kitchen boasts quartz countertops and stainless steel appliances, seamlessly blending style and functionality.

Property Features: 2 split bedrooms and 2 bathrooms; garage; Updated kitchen with quartz counters and stainless steel appliances;Stylish wood laminate flooring throughout; roof less than 3 years old.

Located in Sandy Pines, this home is ideally positioned near the community pool and a short walk to the clubhouse, where you can enjoy Bay Forest’s renowned amenities.

Bay Forest spans 150 acres of natural beauty, bordering the Gulf backwaters. A new $4.5 million boardwalk, which is completed and awaiting final permits, will be the highlight of Bay Forest’s over two miles of walking paths and meander through mangroves to Gulf estuaries.

Resurfaced tennis and pickleball courts (three of each), bocce, and shuffleboard.

Clubhouse Amenities: Social events, fitness center, library, kitchen, bar, and more.

Delnor Wiggins and Barefoot Beaches are just minutes away and it is 30 minutes to Southwest Florida International Airport.

Andrew.Oliver@Compass.com

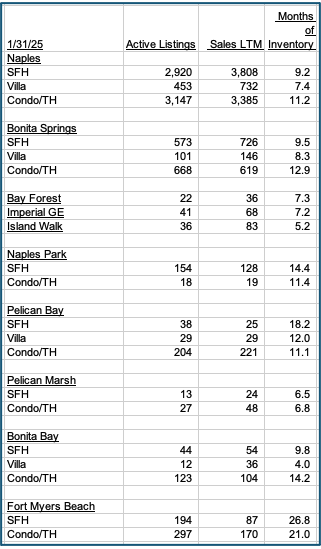

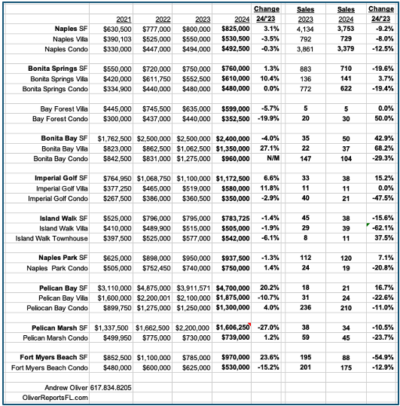

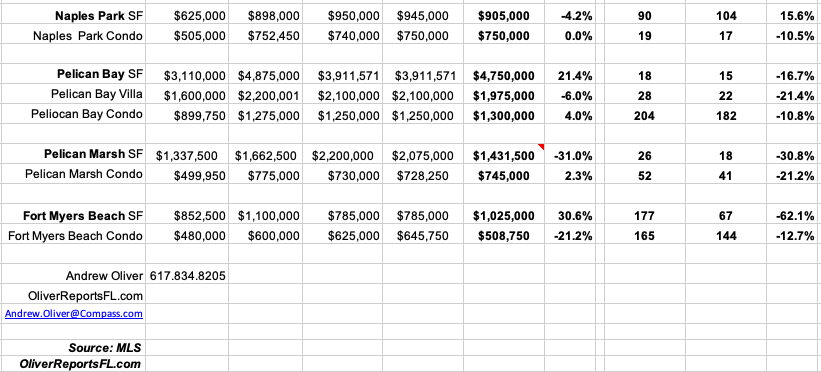

Naples and Bonita Springs 2024 Market Stats

Here are the 2024 Market Stats and 2021-24 comparsions for Naples, Bonita Springs, and selected communities.

Click on the chart to see it in full size.

Andrew.Oliver@Compass.com

Why do people buy New Homes?

Many buyers today flock to newly built homes for several reasons:

1. They simply want NEW. New everything. This can include homes designed for today’s needs and demands, often with finishes, mechanicals, amenities, etc that don’t exist in most existing homes.

2. They don’t wish to undergo a renovation either due to lack of will, or know-how. Most know a renovation is rarely quick, cheap or easy. While an unrenovated home may be far ‘cheaper’, often after a renovation (including the cost of living somewhere while the renovation occurs) the final cost ends up being similar.

3. When you buy brand new, you can finance the entire purchase: property AND renovation (as no renovation is needed). This means you need less cash after closing and may allow you to put down more cash when buying, thereby bringing down monthly expenses/mortgage cost.

4. Every home needs repairs and maintenance over time. Brand new homes too, but often their systems being brand new mean fewer big-ticket repairs/maintenance costs.

5. New homes are built according to new building CODES…. often they are more energy efficient AND resilient. New codes often address the weaknesses of past building codes.

6. Many buyers have shifted their preference to a more modern aesthetic. No, most new buildings are not minimalist, but buyers today often like taller ceilings, bigger windows, open kitchens, bigger bathrooms, etc, the kind of things developers are installing into new homes. This can exist in a sleek all glass box, or a more traditional, even historic-appearing facade.

7. In a FOMO world, brand new can deliver instant gratification. And use. Time Is The Last Luxury.

8. Often hiring a big-name designer of an ultra-luxe building to do one home would be prohibitively expensive: this economy of scale can have real value to those seeking ultra-luxe design.

At COMPASS we have everything from single family starter homes to mansions, condos in 3-unit buildings and townhouses to massive, fully amenitized buildings with hotel services. At all price points, not just those ultra-luxe multi-million-dollar-productions.

Andrew.Oliver@Compass.com

Bay Forest Villas: “Bring me an Offer”

LA JOLLA is a small, lakeside community in Bay Forest with only 8 lakefront, 2- and 3- bed villas.

Number 22, with 3 beds and 3 full baths and 2,127 sq.ft., is currently off market and was last listed at $775,001. There is no other unit in Bay Forest that compares with this one, for location and condition, after the owner has invested some $275,000 in upgrades.

Go HERE to view phtos and videos.

Number 37, a 2-bed plus den, 1,568 sq ft unit, is listed at $579,000.Go HERE to view photos and video.

Contact me on 617.834.8205 to arrange a showing.

With the boardwalk nearing completion, two years after Hurricane Ian, residents will soon to be able to enjoy this great highlight of Bay Forest, with its new kayak launching ramp.

The completion of the boardwalk and the arrival of winter vistors should increase demand in Bay Forest. In anticipation of that, the seller of the Villas would like to have at least one of them sold – so he is open to offers!

Go HERE to view the Bay Forest website, read the latest Newsletter, and watch the 4-minute video of Bay Forest.

And HERE to read the latest news on the Boardwalk.

Bay Forest offers 3 Tennis, 3 pickleball courts, bocce, shuffleboard, fitness center and much more cater to active lifestyles, while the clubhouse, which also has a library, serves as the hub for social events and indoor activities.

Andrew.Oliver@Compass.com

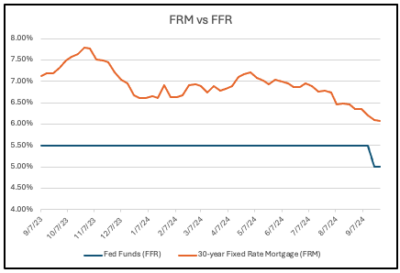

What drives Mortgage Rates – and no it’s not the Federal Reserve

I am always astonished by the number of reports I read, before and after the Federal Reserve (Fed) makes a change in its interest rate, about the effect such a change will have on mortgage rates.

No doubt it came as a surprise to those writers when there was virtually no change in the Freddie Mac weekly survey of mortgage rates this week.

Myth

“Mortgage rates react to the Fed.”

Look at this chart for the last year:

The FFR rate was unchanged at 5.5% for over a year until last week, but during that time frame the FRM varied between a high of almost 7.8% last October and a low of just over 6% last week before the Fed cut its inetrest rate by 0.5%.(The Freddie Mac survey takes place from Monday-Wednesday each week, so the 6.09% reported on September 19 reflected rates before the Fed cut its interest rate).

What happened after the Fed cut rates?

Precious little. The rate before the Fed cut rates was 6.09% and afterwards…. 6.08%.

In simple terms, there is no correlation or link between the Fed’s interest rates and the rate on 30-year Fixed Rate Mortgages.

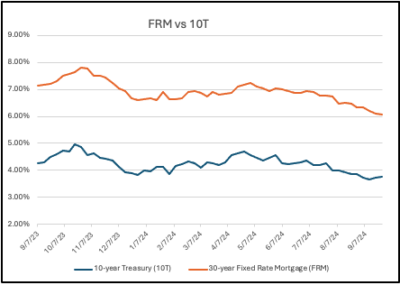

What does determine Mortgage Rates?

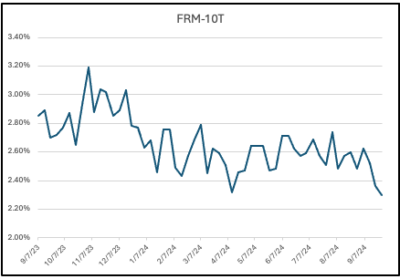

Take a look at this chart which compares the FRM with the yield on the 10-year Treasury note (10T).

Note that the two charts follow each other closely.

Why do Mortgage Rates track the yield on the 10-year Treasury?

Most conventional mortgages (i.e.those meeting the terms set by Fannie Mae and Freddie Mac) are sold by the originator to Fannie and Freddie, thereby freeing up the lenders’ capital to make more loans. Exactly why Fannie and Freddie were founded.

And what do Fannie and Freddie do with these loans? They package them into large pools and sell them to investors in the public market as Mortgage-Backed Securities (MBS). Because investors demand a higher yield to buy MBS than they would to buy a Treasury Note – because the risk is higher – they demand a premium – or spread – above the yield they would receive from the Treasury Note with a similar maturity to the expected life of the mortgages – and that is the 10T.

Is the spread consistent?

Good question. The answer is no.

For most of this century the spread was in the 1.6 – 1.8% range and averaged around 1.75%. The exceptions were:

2008 – the Great Recession and the height of the foreclosure crisis making mortgages unattractive to investors, who demanded higher yields

2020 – at the outset of the pandemic, amidst widespread uncertainty, spreads widened before the Fed started its huge program of pouring money into the economy, buying both Treasuries and MBS and igniting an asset boom

2022-23 – when the Fed finally, belatedly, stopped injecting liquidity into the system, the market reacted to two main factors: the Treasury would need to sell a lot more Securities to fund the spending, and the growing Budget deficit; and the biggest buyer of Treasuries – the Fed itself – was switching from being a buyer to a seller.The Fed also continues to hold a huge amount of MBS, which it is slowly reducing by not reinvesting.

Fannie and Freddie have increased fees to lenders

In addition to the fact that the Budget deficit continues to increase, while the Fed has been a seller of Treasuries, Fannie and Freddie have increased the fees they charge to lenders. These two factors have combined to increase the spread to more than the historic 1.6-1.8% , as shown in this chart, again for the last year:

Where are Mortgage Rates headed?

Thw two biggest questions facing the Treasury market are: will Congress take steps to rein in the soaring Budget deficit, and will foreign investors retain their appetite for US securities?

I don’t know, but to know where mortgage rates are headed,the most important number to watch is the yield on the 10-year Treasury Note.

Cheaper Mortgages are available

The Freddie Mac weekly survey is a national report. I work with lenders in both Florida and Massachusetts who are offering 30-year FRM for 5.5%. And other options are as low as 5%. Call me for details.

Recent Market Reports

Naples Mid-Year 2024 Market Report

Bonita Springs Mid-Year 2024 Market Report

Fort Myers Beach Mid-Year 2024 Market Report

Please contact me for a market report that includes properties in your area which were recently listed or sold.

Economic and mortgage commentary

The Federal Reserve’s new buzzword: Recalibrate

Federal Reserve Chair Powell:The Time has Come

Earth to Federal Reserve: What are you waiting for?”

The Federal Reserve’s Analysis Paralysis

Andrew.Oliver@Compass.com

The Federal Reserve’s new buzzword: Recalibrate

At Wednesday’s press conference after the Fed – finally – cut rates by 50 basis points (bp)(0.5%) – Fed Chair Powell introduced a new phrase to explain their action: “recalibrate.”

We have been through “transient inflation”; “data dependent”; “higher for longer”; and “data-dependent, not data point dependent” and have reached “recalibrate”.

Chair Powell denied that they were playing catch up because they waited too long to start cutting rates (they are, and they did).

Frankly, after their slow and deliberate approach this year, I expected only 25 bp. BUT…the next meeting is not until November 6, the day after the Election. And who knows what the environment will be on that date? It is certainly not out of the question that there will be a lack of clarity about the outcome. And while the Fed states that it not influenced by political considerations, they will naturally be aware of an environment which may well make it difficult for them to make an accurate forecast of the future.

So 50 bp now is “not a catch up” – but it would have been more consistent – and raised fewer questions – if they had cut 25 bp in July and a further 25 bp now.

Mortgage rates

I will update my 2023 article Why Mortgage Rates will fall in 2024 in the next few days. In that article I predicted that the 30-year Fixed Rate Mortgage (FRM) would drop below 6% by the end of 2024. I also explained why mortgage rates do not follow the Federal Reserve’s interest rate decisions, but are market driven based on the yield of the 10-year Treasury.

And to make to make that point more clearly: in both Massachusetts and Florida it is already possible to get FRMs for 5.5%, a sharp drop from from earlier in the year.

Recent Market Reports

Naples Mid-Year 2024 Market Report

Bonita Springs Mid-Year 2024 Market Report

Fort Myers Beach Mid-Year 2024 Market Report (more…)