Are mortgage rates heading up or down?

For several years “experts” have been forecasting that mortgage rates were about to rise, but forecasts of an imminent end to low rates are reminiscent of Mark Twain’s alleged comment that reports of his death had been greatly exaggerated.

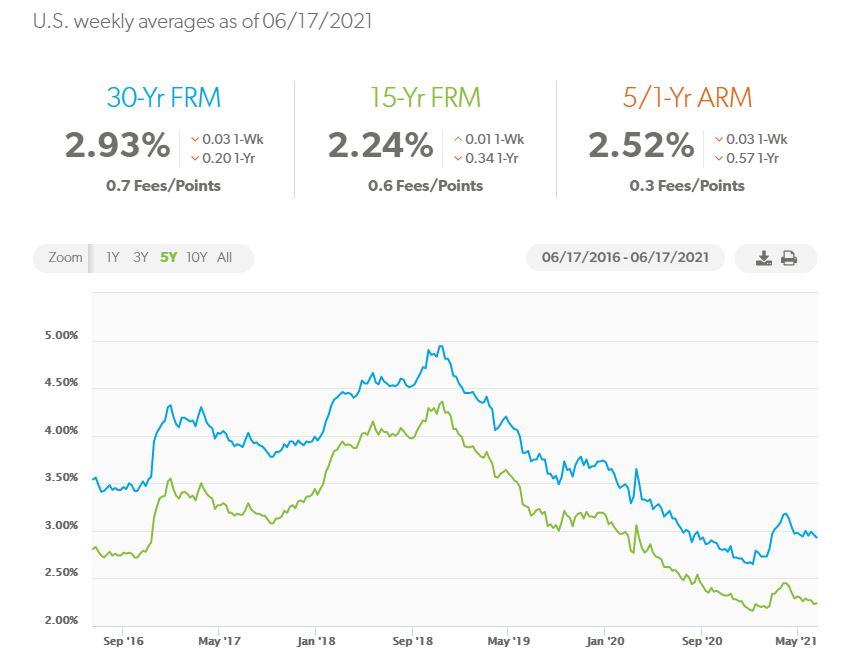

The 30-year Fixed Rate Mortgage (FRM) reached almost 5% in November 2018, but since then has been in an almost uninterrupted downward trend, with a few short-lived spikes upwards:

Which brings us to the question: is the next move going to be

Inflation

The main economic debate affecting mortgage rates is whether the current surge in consumer prices is, as the Federal Reserve believes, “transient”, or as many economists believe more ingrained into the system.

A lot of talk has been about the huge increase in lumber prices, which affects the cost of new home construction, and the recent sharp decline in prices. “Our expectation is that these high-inflation readings that we are seeing now will start to abate. And it’ll be like the lumber experience,” (Federal Reserve Chair Powell told reporters on Wednesday. “Prices that have moved up really quickly because of the shortages and bottlenecks and the like, they should stop going up. And at some point, they, in some cases, should actually go down. And we did see that in the case of lumber.”

Econbrowser

Econbrowser

According to the Federal Reserve Bank of New York’s Survey of Consumer Expectations for May, however, the expectation is that the inflation rate will be up to 4% one year from now — a new high for one-year-ahead inflation expectations — and at 3.6% three years from now, the highest level since August 2013.

Should inflation prove to be more persistent than the Fed expects, then it is likely that the Fed will have to start to increase interest rates sooner and move them up more quickly than it currently expects. And mortgage rates would follow.

The Fed’s dual mandate

The Fed’s two goals of price stability and maximum sustainable employment are known collectively as the “dual mandate.” In explaining its policy of keeping interest rates low – in part by buying large quantities of Treasuries and Mortgage-Backed Securities, the latter helping to keep mortgage rates low – the Fed refers to the still high level of unemployment.

I have to admit that I struggle to understand how low interest rates, which boost asset classes such as stock prices and real estate, are helping to boost employment. “Trickle-down” is the economic proposition that taxes on businesses and the wealthy in society should be reduced as a means to stimulate business investment in the short term and benefit society at large in the long term. In recent years we have had the Reagan and Bush tax cuts and the 2017 tax Cuts and Jobs Act. It is hard to be confident that these cuts have made a substantial contribution to the betterment of the least fortunate and lowest earning in our society.

Lower interest rates also benefit those who own assets which appreciate. Meanwhile, higher unemployment benefits – albeit temporary- have at least some drag effect on encouraging people to return to work.

I would like to see the Fed start to reduce (taper) its bond buying, while encouraging Congress to focus on removing barriers to employment – by providing increased child care allowances, for example. In other words, deal directly with the problem rather than hoping that benefits will trickle down somehow.

But…..I don’t have a seat on the Federal Reserve Board and so we will have to wait until those who do decide the time is right to start raising interest rates. Meanwhile, as I have mentioned many times in these posts, mortgage rates are historically extremely low. The challenge remains finding a house to buy.

And read these recent articles:

Hello sub 3% mortgages – again

A Pre-Qualification Letter Doesn’t Equal Being Pre-Approved

“Party on, dude” says the Federal Reserve

It’s 80 degrees in Florida….

If you – or somebody you know – are considering buying or selling a home and have questions about the market and/or current home prices, please contact me on 617.834.8205 or Andrew.Oliver@SothebysRealty.com.

Andrew Oliver

Sales Associate | Market Analyst | DomainRealty.com

REALTOR®

Naples, Bonita Springs and Fort Myers

Andrew.Oliver@DomainRealtySales.com

m. 617.834.8205

www.AndrewOliverRealtor.com

www.OliverReportsFL.com

“If you’re interested in Marblehead, you have to visit the blog of Mr. Andrew Oliver, author and curator of Oliver Reports . He’s assembled the most comprehensive analysis of Essex County we know of with market data and trends going back decades. It’s a great starting point for those looking in the towns of Marblehead, Sale, Beverly, Lynn and Swampscott.”

Andrew Oliver

Market Analyst | Team Harborside | teamharborside.com

REALTOR®

Sagan Harborside Sotheby’s International Realty

One Essex Street | Marblehead, MA 01945

m 617.834.8205

www.OliverReports.com

Andrew.Oliver@SothebysRealty.com

Sotheby’s International Realty® is a registered trademark licensed to Sotheby’s International Realty Affiliates LLC. Each Office Is Independently Owned and Operated

[…] 30-year Fixed Rate Mortgage ticked back up to 3% this week. I re-read Are Mortgage Rates headed Up or Down? which I published in June and I still think it summarises the situation quite well. Hence I have […]

[…] Are mortgage rates heading up or down? Buyers are overpaying, but are there signs of a bubble? […]

[…] articles: Are mortgage rates heading up or down?” Hello sub 3% mortgages – again A Pre-Qualification Letter Doesn’t Equal Being Pre-Approved […]

[…] Naples rated No. 1 beach town to live in Where are mortgage rates headed? […]

[…] Where are mortgage rates headed? Naples market summary in June […]

[…] Are mortgage rates heading up or down?” Naples Housing Market in May “Party on, dude” says the Federal Reserve Buyers are overpaying, but are there signs of a bubble? Will the Housing Market Frenzy Die Down? That Depends on Sellers […]

[…] Are mortgage rates heading up or down? Buyers are overpaying, but are there signs of a bubble? “Party on, dude” says the Federal Reserve Hello sub 3% mortgages – again It’s 80 degrees in Florida…. […]

[…] articles: Are mortgage rates heading up or down?” Hello sub 3% mortgages – again A Pre-Qualification Letter Doesn’t Equal Being Pre-Approved […]