Mortgage rates back to 3% – again

The 30-year Fixed Rate Mortgage ticked back up to 3% this week. I re-read Are Mortgage Rates headed Up or Down? which I published in June and I still think it summarises the situation quite well. Hence I have included the link rather than repeating the arguments.

The proximate cause for the increase in mortgage rates this week was the increase in the yield on the US Treasury 10-year Note. The increase started last week (after the Freddie Mac weekly survey, which is collected from Monday-Wednesday) when the Federal Reserve (Fed) confirmed that, if current trends continue, it will start to reduce its purchases of both Treasuries and Mortgage Backed Securities (MBS) soon and aim to end purchases by the middle of 2022.

At the same time, we saw a rate increase in Norway – the first in Europe- following earlier increases in Brazil and South Korea. And while the Fed continues to state that it will not consider actual rate increases (I am not sure why they refer to it as “lift off”- sounds like rocket-speed increases which it will not be) until after the end of the bond purchases, investors noticed a shift in the number of members forecasting a rate increase in 2022 rather than 2023.

And inflation continues to run hot. The Fed thinks this is transitory, but many others fear that it will be sustained forcing the Fed to raise rates sooner than it currently anticipates.

The Numbers

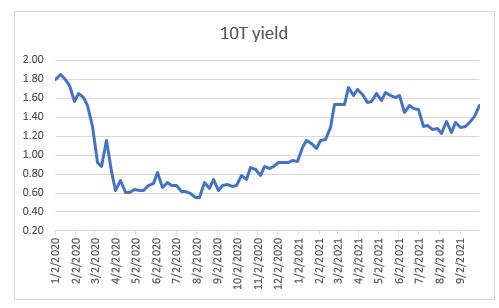

This is the yield on the 10-year Treasury(10T) since the beginning of 2020. The Federal Reserve’s huge purchases drove rates down sharply at the outset of the pandemic. Since the middle of 2020 rates have been on a rising trend – but are still below the pre-COVID levels:

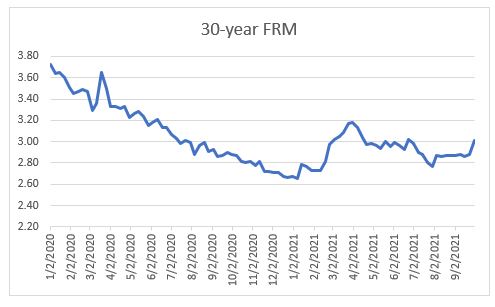

Mortgage Rates

Because mortgage rates are driven by the yield on 10T, the FRM dropped from 3.7% at the start of 2020 to 2.7% at the end of that year.

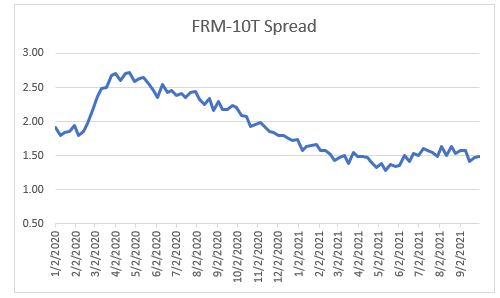

The spread – the difference between FRM and 10T – was very steady on average at around 1.7% from 2005 to 2019, with the exception of the Great Recession when the spread jumped because investors were wary about buying mortgages in fear of a wave of defaults. This fear returned with the pandemic, driving up the spread again in 2020, and gradually dissipated as the year progressed.

Comment

While the spread between FRM and 10T has been hovering around the 1.5% level this year, that is below the long-term average of 1.7%. And the reason is that the Fed’s buying of MBS is estimated to be keeping mortgage rates about 1/4% below where they would otherwise be. So add 0.25% to 1.5% and we are pretty well in line with long-term, stable market spreads.

In other words, markets have returned to a more normal condition – which is why I wrote in June:

“I have to admit that I struggle to understand how low interest rates, which boost asset classes such as stock prices and real estate, are helping to boost employment. “Trickle-down” is the economic proposition that taxes on businesses and the wealthy in society should be reduced as a means to stimulate business investment in the short term and benefit society at large in the long term. In recent years we have had the Reagan and Bush tax cuts and the 2017 tax Cuts and Jobs Act. It is hard to be confident that these cuts have made a substantial contribution to the betterment of the least fortunate and lowest earning in our society.

Lower interest rates also benefit those who own assets which appreciate. Meanwhile, higher unemployment benefits – albeit temporary- have at least some drag effect on encouraging people to return to work.

I would like to see the Fed start to reduce (taper) its bond buying, while encouraging Congress to focus on removing barriers to employment – by providing increased child care allowances, for example. In other words, deal directly with the problem rather than hoping that benefits will trickle down somehow.

But…..I don’t have a seat on the Federal Reserve Board and so we will have to wait until those who do decide the time is right to start raising interest rates. Meanwhile, as I have mentioned many times in these posts, mortgage rates are historically extremely low. The challenge remains finding a house to buy.”

I haven’t changed my opinion and I still don’t have a seat at the Fed.

And I haven’t changed my view that mortgage rates are historically very cheap:

Or that the main challenge is finding a house to buy.

Read these recent articles:

Naples Housing Market August Review

Yes Virginia, it is Still a Sellers’ Market

Andrew Oliver

REALTOR®| Market Analyst | DomainRealty.com

Naples, Bonita Springs and Fort Myers

Andrew.Oliver@DomainRealtySales.com

m. 617.834.8205

www.AndrewOliverRealtor.com

www.OliverReportsFL.com

_____________

Market Analyst | Team Harborside | teamharborside.com

Sagan Harborside Sotheby’s International Realty

One Essex Street | Marblehead, MA 01945

www.OliverReportsMA.com

Andrew.Oliver@SothebysRealty.com

Sotheby’s International Realty® is a registered trademark licensed to Sotheby’s International Realty Affiliates LLC. Each Office Is Independently Owned and Operated

[…] Bonita Springs/Estero Area and Community Market Reports Sanibel/Captiva Q3 2021 Market Report Mortgage rates back to 3% – again Foreign Buyers May Return in […]

[…] Yes Virginia, it is Still a Sellers’ Market Foreign Buyers May Return in November Mortgage rates back to 3% – again […]

[…] these recent articles: Naples Housing Market August Review Mortgage rates back to 3% – again Yes Virginia, it is Still a Sellers’ […]