Adjustable-Rate Mortgages Staging a Comeback

Applications for Adjustable-rate mortgages (ARMs) increased 12.5% year-to-year for the week ending June 18, according to the Mortgage Bankers Association (MBA), as the discount from the 30-year FRM has widened in recent weeks.

ARMs dropped in popularity after the 2008 financial crisis, but they are starting to reemerge as buyers contend with record high home prices. “The epic surge in home prices has people looking to save money on monthly payments anywhere they can,” says Matt Graham, chief of operations at Mortgage News Daily.

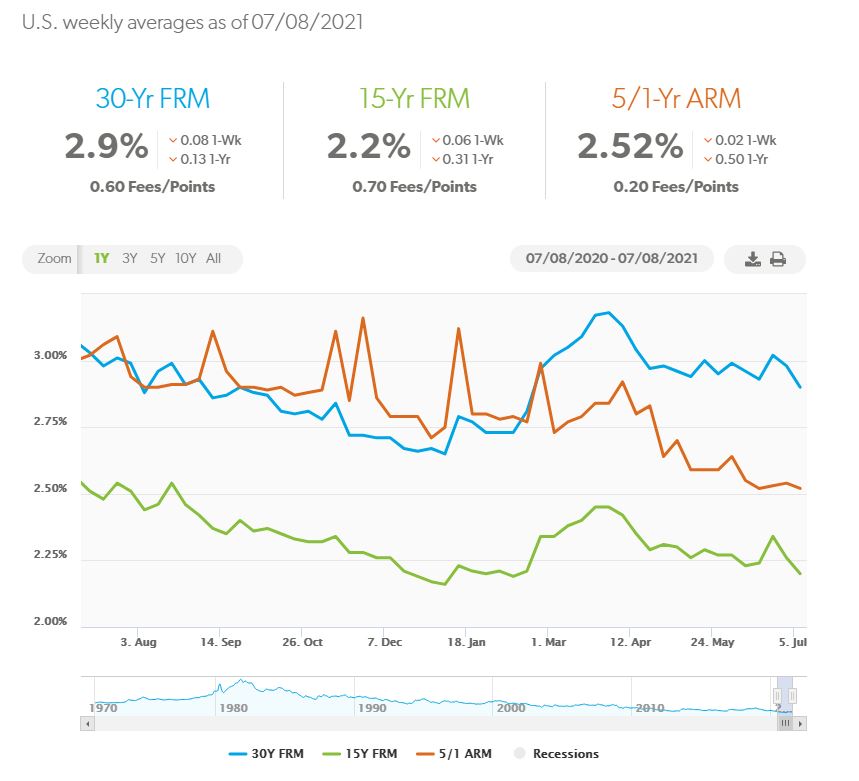

Source: Freddie Mac

With an ARM, buyers usually get a lower mortgage rate. In exchange, however, they also agree that the rate can go up (or down) after a set number of years, usually five or 10. If national mortgage rates go up in that time, they’ll likely face higher monthly mortgage payments. Given today’s historically low mortgage rates, that means today’s FRM borrowers will be paying more when their loan adjusts at some future date.

Some borrowers may think they’ll refinance to a fixed-rate mortgage or move before the loan adjusts. Some may assume they’ll be in a better financial position to pay a higher amount five or 10 years in the future. For still others, the lower rate offered via an ARM may be their only option if they want to buy rather than rent.

Still, lenders say that only the most qualified borrowers are getting approved for ARMs; they tend to have higher credit scores and put more money down than fixed-rate mortgage borrowers. There is also more education around these loans than in the days of the financial crisis. Interest-only ARMs are also less prevalent. (With an interest-only ARM, borrowers don’t start paying anything toward their principal until a time established in the loan documents.)

ARMs are a relatively small part of the mortgage market, comprising just 3.6% of applications for the week ending June 25, according to the Mortgage Bankers Association.

In general, financial experts say ARMs are less useful if homeowners plan to stay in their homes for decades. But for those who plan to stay in their homes for less time, ARMs may be a more attractive option.

ARMs are most popular among borrowers seeking higher-priced mortgages. The average ARM loan size was $904,000 compared to $317,500 for a fixed-rate loan for the week ending June 25, according to the MBA’s data.

While ARMs got a bad name during the financial crisis, I have long believed that they are a useful tool as part of overall financial planning for those who understand the risks. That the average ARM was $904,000 in the recent period confirms that they are being used by sophisticated borrowers.

And read these recent articles:

Naples market summary in June

Naples rated No. 1 beach town to live in

Where are mortgage rates headed?

Bonita Springs-Estero May Housing Market review

Fort Myers May Housing Market report

It’s not a bubble unless it pops

Andrew Oliver

Sales Associate | Market Analyst | DomainRealty.com

REALTOR®

Naples, Bonita Springs and Fort Myers

Andrew.Oliver@DomainRealtySales.com

m. 617.834.8205

www.AndrewOliverRealtor.com

www.OliverReportsFL.com

________

“If you’re interested in Marblehead, you have to visit the blog of Mr. Andrew Oliver, author and curator of Oliver Reports . He’s assembled the most comprehensive analysis of Essex County we know of with market data and trends going back decades. It’s a great starting point for those looking in the towns of Marblehead, Sale, Beverly, Lynn and Swampscott.”

Andrew Oliver

Market Analyst | Team Harborside | teamharborside.com

REALTOR®

Sagan Harborside Sotheby’s International Realty

One Essex Street | Marblehead, MA 01945

m 617.834.8205

www.OliverReports.com

Andrew.Oliver@SothebysRealty.com

Sotheby’s International Realty® is a registered trademark licensed to Sotheby’s International Realty Affiliates LLC. Each Office Is Independently Owned and Operated

[…] Where are mortgage rates headed? Naples market summary in June Bonita Springs June Housing Market Summary Adjustable-Rate Mortgages making a comeback […]