Why Mortgage Rates Will Fall

I have read and heard several comments suggesting that the increase in the 30-year Fixed Rate Mortgage (FRM) this year has been a direct result of the increase in the Federal Reserve’s Fed Funds rate (FF).

This is not correct.

As I will demonstrate, the FRM is determined by market forces, and in particular by the extra yield – the “spread” – which investors require when buying pools of mortgages (Mortgage Backed Securities or MBS), as compared with the risk-free yield available with the 10-year Treasury Note (10T) which has the nearest duration to the expected life of a pool of mortgages.

In contrast, the FF is the rate that banks use when setting their Prime Rates. When the FF increases, banks increase their Prime Rates and therefore the interest rate on those loans whose rates are based upon Prime Rates – e.g. credit cards and auto loans.

And we will see that the FRM increased this year long before the Fed started to increase the FF rate.

Mortgage-Backed Securities (MBS)

A conventional mortgage or conventional loan is any type of home buyer’s loan that is not offered or secured by a government entity. Instead, conventional mortgages are available through private lenders, such as banks, credit unions, and mortgage companies.

Most conventional mortgages are packaged into mortgage-backed securities and sold to investors. This allows the bank or originator to use its capital to finance more mortgages.

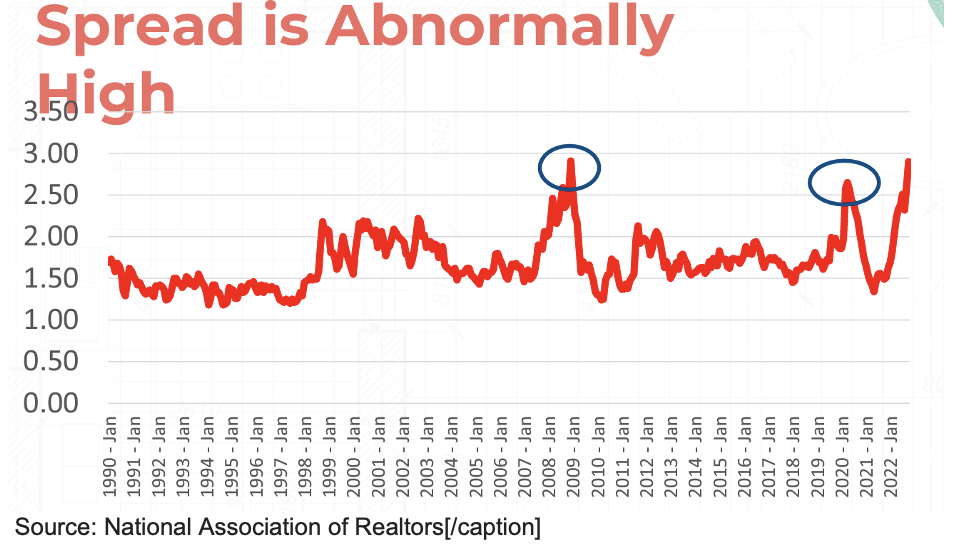

The relationship between 10T and FRM

This chart shows how the two have moved in lockstep over the last 30-plus years:

Source: National Association of Realtors

While the “spread” has mostly been in the 1.5-2% range, it has fluctuated, especially during times of financial stress or uncertainty:

2008-2009

During the great recession at the end of the sub-prime mortgage boom, home prices dropped sharply. Fearing that some mortgages would not be repaid in full, MBS investors demanded a higher yield to compensate – they hoped – for the extra risk – and the spread increased to 3%.

2020

The increase in the spread in the early months of the COVID-19 outbreak was caused by a different dynamic. In order to ensure the continued functioning of financial markets, the Federal Reserve slashed interest rates close to zero and at the same time embarked upon a massive buying program for both Treasury securities and MBS. The yield on Treasuries was driven down more than on MBS, leading to an increase in the spread to 2 3/4%.

2022

At the beginning of 2022 the spread was 1.6%, well within its historic range. The spread then increased to 2% in March, to 2.6% in June and by October it had reached 3%. Which means that the FRM was 1.4% higher than it would have been had the spread been the same as it was at the beginning of the year.

There is, unfortunately, no simple answer as to why the spread has increased so dramatically in 2022, but some of the factors include: fears of a recession and the impact that may have on home prices; the unpredictable volatility in interest rates (as an example, until very recently some financial analysts were predicting that the yield on 10T would reach 5% – and then two reports hinted at an easing of inflation and the yield dropped back to 3.5%); the Fed’s plans to reduce its holdings of MBS (it owned 30% of outstanding MBS at the peak); the substantial drop in refinancing activity; and the increased cost of funds for lenders as they have to compete for deposits with the higher-yields available on CDs and Tresuries.

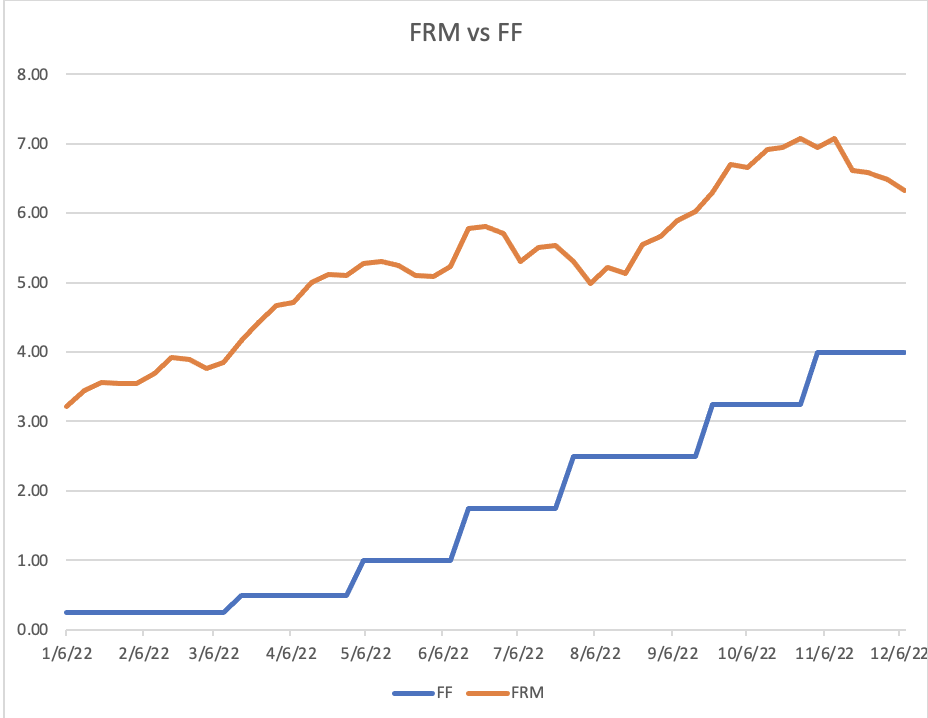

No correlation between FRM and FF

As the chart below shows, the FRM increased from 3% to 4% before the Fed made its first increase of just 1/4%. And the rate reached 5% before the Fed increased the FF again.

On the downside, the FRM dropped 3/4% in July at a time when the FF increased by 3/4%. And finally, in the last month the FRM has dropped by 3/4% with no change in the FF rate and with expectation of a further increase in the FF rate in mid-December.

Source: Freddie Mac, US Treasury

When will mortgage rates drop?

We have already seen a drop of more 3/4% in the FRM, but the spread still remains elevated at around 3%. History gives us every reason to believe that the spread will eventually drop back to a more normal level. What is not clear is where the yield on 10T will be: on one day recently one investment bank forecast a 2023 year- end 10T yield of 2.5% – and another 4.75%!

But bear in mind that even if the yield does reach 4.75%, a return to a more normal spread would leave the FRM at around today’s levels.

Investment banks are paid to make forecasts which have so many assumptions and variables that they are really no more than reasoned guesses. I would only say that I am more confident of the destination than I am of the time it will take to get there. Rather like flying these days.

And read these recent articles:

Buyers Undeterred in Ian’s Hardest-Hit Areas

Home Prices After Ian? Probably Going Up

How have home prices behaved after previous major Hurricanes?

How to protect your house from title fraud

Florida Lawmakers Pass Insurance, Condo Reforms

Florida Regulator: Insurers Can Offer Roof Deductibles

Expansion Plans for Fort Myers Airport

Guide to Buying and Selling in Southwest Florida

Market Summaries

Florida Market Update in 4 minutes

Sales Resemble Pre-Pandemic — But Not Pricing & Inventory

- Andrew Oliver, M.B.E., M.B.A.

Real Estate Advisor

Andrew.Oliver@Compass.com

m 617.834.8205

[…] and Economic commentary Why Mortgage rates Will Fall What drives Mortgage Rates in one chart Lies, Damned Lies and Inflation […]

[…] and Economic commentary Why Mortgage rates Will Fall What drives Mortgage Rates in one chart Lies, Damned Lies and Inflation […]

[…] and Economic commentary Why Mortgage rates Will Fall What drives Mortgage Rates in one chart Lies, Damned Lies and Inflation […]

[…] and Economic commentary Why Mortgage rates Will Fall What drives Mortgage Rates in one chart Lies, Damned Lies and Inflation […]

[…] and Economic commentary Why Mortgage rates Will Fall What drives Mortgage Rates in one chart Lies, Damned Lies and Inflation […]

[…] read these articles: Mortgage and Economic commentary Why Mortgage rates Will Fall What drives Mortgage Rates in one chart Lies, Damned Lies and Inflation […]

[…] read these recent articles: HOW AND WHEN WILL HOUSING REBOUND? Why Mortgage rates Will Fall Buyers Undeterred in Ian’s Hardest-Hit Areas Home Prices After Ian? Probably Going Up How have […]

[…] For a more detailed explanation of what drives mortgage rates – and they the FRM will fall at some point – read Why Mortgage Rates Will Fall […]

[…] read these recent articles: HOW AND WHEN WILL HOUSING REBOUND? Why Mortgage rates Will Fall Buyers Undeterred in Ian’s Hardest-Hit Areas Home Prices After Ian? Probably Going Up How have […]

[…] Damned Lies and Inflation “Statistics”* HOW AND WHEN WILL HOUSING REBOUND? Why Mortgage rates Will Fall Buyers Undeterred in Ian’s Hardest-Hit Areas Home Prices After Ian? Probably Going Up How have […]

[…] read these recent articles: Why Mortgage rates Will Fall Buyers Undeterred in Ian’s Hardest-Hit Areas Home Prices After Ian? Probably Going Up How have […]

[…] read these recent articles: Why Mortgage rates Will Fall Buyers Undeterred in Ian’s Hardest-Hit Areas Home Prices After Ian? Probably Going Up How have […]

[…] read these recent articles: Why Mortgage rates Will Fall Buyers Undeterred in Ian’s Hardest-Hit Areas Home Prices After Ian? Probably Going Up How have […]

[…] these recent articles: Why Mortgage rates Will Fall Buyers Undeterred in Ian’s Hardest-Hit Areas Home Prices After Ian? Probably Going Up How have […]

[…] these recent articles: Why Mortgage rates Will Fall Buyers Undeterred in Ian’s Hardest-Hit Areas Home Prices After Ian? Probably Going Up How have […]