Are Mortgage rates really under 3%?

When Freddie Mac released its weekly mortgage survey on Thursday it did so with the heading: “Mortgage Rates Drop Below Three Percent Again.”

Which they are not now.

The problem lies with the methodology. Freddie Mac surveys lenders from Monday to Wednesday with the major weighting given to Monday’s rates. As I have explained in many postings over the years (see Mortgage Rates back to 3% – again as an example), the 30-year Fixed Rate Mortgage (FRM) is priced based upon a premium that investors, when they buy pools of mortgages, demand over the yield on the nearest-equivalent US Treasury – which is the 10-year Note (10T). Thus, if the yield on 10T increases from Monday to Thursday – as it did this week – by the time of Thursday’s announcement the FRM may have changed – as it did this week.

Mortgage News Daily had a great article this week and I am going to use their charts. I recommend signing up for their newsletter, a source of great information and opinion.

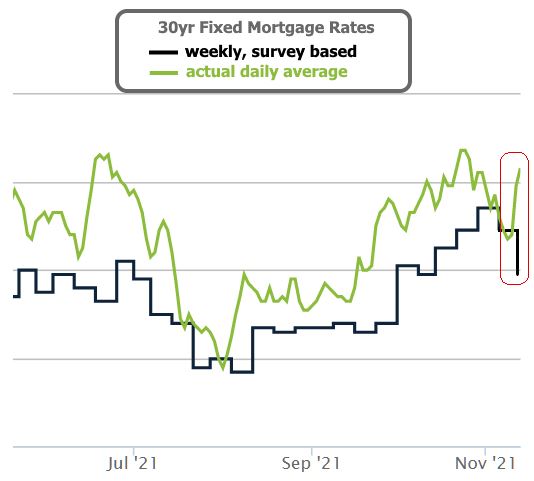

Mortgage Rates

The first chart shows the divergence at the end of the week between the Survey number and the actual market:

Mortgage News Daily

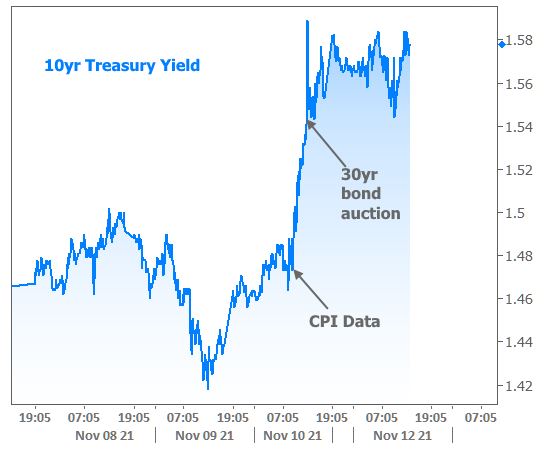

And what drives this is the movement in the 10T market, where yields spiked after the release of the CPI numbers on Wednesday:

Mortgage News Daily

Where is Inflation headed?

That, of course, is the biggest economic question facing the mortgage market and indeed the economy. Is it transitory, episodic or somewhat longer-lasting?

The Federal Reserve – you know, the body whose opinion actually matters – has talked of “upward pressure on prices from the rebound in spending,” particularly with the supply problems. “However, these one-time increases in prices are likely to have only transitory effects on inflation.”

This month the Fed tweaked its policy statement to note that inflationary pressures are not “transitory” but “expected to be transitory,” and that bottlenecks would last “well into next year” before fading.

This week Atlanta Fed President, Raphael Bostic, said that instead of describing the coronavirus “pandemic-induced price swings” as “transitory,” United States Federal Reserve officials should use the word “episodic” to characterize current inflation developments.

“By episodic, I mean that these price changes are tied specifically to the presence of the pandemic and, once the pandemic is behind us, will eventually unwind, by themselves, without necessarily threatening longer-run price stability,” Bostic said at a virtual event organized by the Peterson Institute for International Economics.

Bostic also noted that “severe and pervasive” disruptions with supply chains, the main causes of the high inflation rate, “will probably last longer than most of us initially expected.” In addition, he pointed out that underlying inflation is “indeed above the [Federal Open Market] Committee’s 2% objective.”

The Federal Reserve’s actions

If a major fire is described as a 5-alarm fire, what the Federal Reserve faced in March 2020 was about a 50-alarm fire. Its immediate and huge response undoubtedly saved the US – and the world – from a depression, while the buying of mortgage-backed securities (MBS) unfroze that market and allowed residential sales to close.

But that was 18 months plus ago. The Fed has finally started to slow its monthly purchases of Treasuries and MBS, but it will still be making some purchases for several more months, injecting more cash into the financial system. For several months I and many others have argued that the Fed should cease these emergency activities and move more quickly to raising interest rates – which is has said it will not consider until after it ends its purchases next June.

Economist Milton Friedman famously said that “inflation is always and everywhere a monetary phenomenon. The more money that is circulating in an economy chasing limited goods and services, the higher inflation is likely to be.”

The stock market and housing prices

We have seen that money chases asset prices – the stock market and residential housing – to record levels, while banks have been encouraging their larger customers not to deposit funds with them.

The fear is that, should inflation prove to be longer-lasting than the Fed hopes, it will be forced to raise rates more quickly than it would like, in order to bring inflation under control, and that could trigger a recession.

I can ask where inflation is headed but I cannot provide a better answer than anybody else – I don’t know. Normally, a time of uncertainty leads to a sell off in markets – but as you have noticed times are not normal. The stock market is driven in large party by TINA (There Is No Alternative) while the housing market still lacks the supply of homes necessary to meet demand – and that is without considering the pandemic-induced changes in attitudes as people reconsider their lifestyle (“I can work from anywhere, so why not a low-tax, warm-weather State?) or indeed a lot of 50-55-year-olds deciding that they can afford to retire and are not going to return to the workforce – or at least not until they get bored in retirement.

In 2002 Defense Secretary Donald Rumsfeld said: “there are known knowns; there are things we know we know. We also know there are known unknowns; that is to say we know there are some things we do not know. But there are also unknown unknowns—the ones we don’t know we don’t know. And if one looks throughout the history of our country and other free countries, it is the latter category that tends to be the difficult ones.”

It may take a major “unknown unknown” to end the current boom in both the stock market and housing market. The stock market is more sensitive to interest rates than the housing market: we invest savings n the stock market; we buy a house to live in – for the most part, at least.

Supply and demand

This very simple equation continues to be the most important in the housing market. Supply remains extremely low and demand high. From time to time sellers will get overly optimistic and try to push prices too far too quickly. But reasonably-priced properties continue to see very strong demand. And whether the FRM is 3% or indeed 3.5% or 4%, mortgages are still very cheap.

Read these articles about the impact European – and Canadian – buyers will have on the real estate market:

The Europeans have started to Arrive

Travelers are returning to Southwest Florida to find low inventory

International Tourism to Return to Southwest Florida

And these market reports:

Naples area Fall Market Reports

Bonita Springs/Estero Area and Community Market Reports

Sanibel/Captiva Q3 2021 Market Report

Andrew Oliver, M.B.E., M.B.A.

Real Estate Advisor

Andrew.Oliver@Compass.com

www.TheFeinsGroup.com

www.OliverReportsFL.com

Compass

800 Laurel Oak Drive, Suite 400, Naples, FL 34108

m: 617.834.8205

Licensed in Massachusetts

www.OliverReportsMA.com

[…] Florida The Europeans have started to Arrive Florida Dodges Bullet as Storm Season Set to End Are Mortgage Rates really under 3%? How accurate are Zillow’s […]