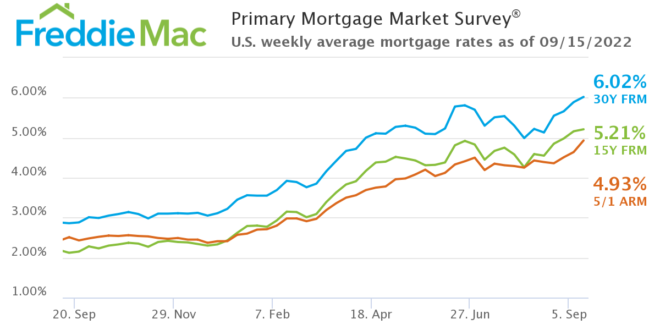

Mortgage Rates peaked? I spoke too soon

In June I published Have Mortgage Rates peaked? when the 30-year national average Fixed-Rate Mortgage (FRM) reached 5.81% and commented: “..a realistic expectation would be that the spread (the difference between the FRM and the yield on the 10-year Treasury) will drop from its current 2.5% to at least 1.8% at some point. If the yield on 10T stays in the low 3% range that would suggest that the FRM will drop below 5% again.”

Well it did…for a while, dropping to 4.99% on August 4th.

But then this happened:

Why have mortgage rates jumped again?

A lot of press and industry commentary relates the increase in the FRM to the increases in the Federal Reserve’s Fed Fund Rate (FFR). In fact, the FFR is used by banks to set their prime rates, used in calculating the interest rate on credit cards and auto loans, while the FRM is based upon the market appetitie for mortgage-backed securities (MBS). Conventional mortgages – those backed by Freddie Mac and Freddie Mae – are packaged and sold to investors. And those investors consider the yield offered by the US Treasury with the closest life to that expected by mortgages – the 10-year (10T)- and then demand an extra yield – the spread referred to above – to compensate fore the additional risk in buying mortgages rather than securities with the full faith of the US Government.

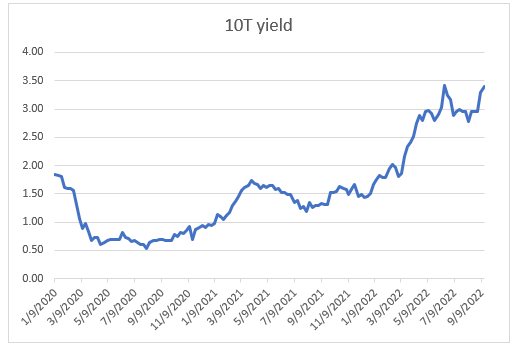

The yield on the 10-year Treasury dropped sharply for a while but has since rebounded again close to the June high:

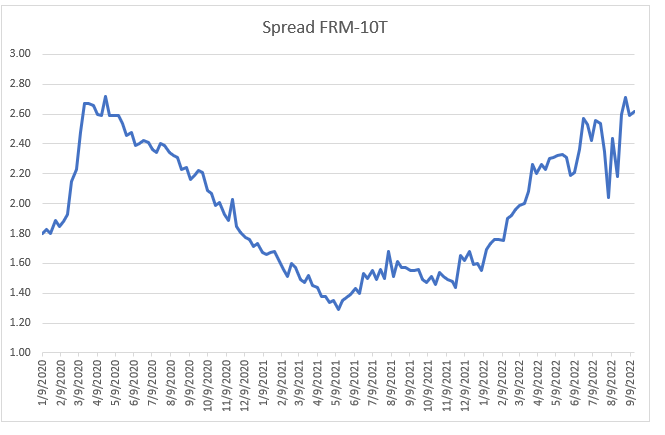

While the spread, after falling to close to 2%, has also rebounded:

So what happened?

In Federal Reserve tries to rewrite history published on July 30th, I commented, after Fed Chairman Powell’s press conference: “So this week the stock market has decided that by the time the Fed meets again in September the economy will have slowed so much that the Fed will be able to ease off on its interest rate increases. Hence the big rally as “risk on” returns, betting that we will actually have a soft landing for the economy based upon the continuing strength of the labor market.

Or maybe it was just a strong, bear market rally from an oversold position where “everybody” was negative.”

The stock market rally lasted for a while, but then the market got the very short message delivered by Powell at Jackson Hole on August 26. In essence, he told the market that those betting that the Fed would either pause interest rate increases or reverse them quickly needed to “read my lips.” The Fed was going to continue to increase rates and tighten monetary policy until inflation returned to its 2% target.

Since then, the stock market has fallen again, and yields have soared.

And mortgage rates have been hit with a double whammy: higher 10-T yields and wider spreads.

Where to now?

When my daughter was growing up I used to tell her that it was always important to understand the difference between relative and absolute. In relative terms, the spread between the FRM and 10T is unusually high and at some point this should return to the norm. In absolute terms, whether or not this means that the FRM will be lower depends upon the yield on the 10T.In the meanwhile, those buying a house now might want to discuss with their financial adviser whether an Adjustable Rate Mortgage – I like the 7-year fixed option – would be appropriate.

And read these recent articles:

Economic commentary

No, the Federal Reserve does not control mortgage rates

Federal Reserve tries to rewrite history

Has Inflation Peaked?

Have Mortgage Rates peaked?

Are we already in a Recession?

Federal Reserve in Fantasyland: Implications for Housing Market

How far Behind the Curve is the Federal Reserve?

Will the Federal Reserve show chutzpah today?

Why are Mortgage Rates so high?

Other

How to protect your house from title fraud

Florida Lawmakers Pass Insurance, Condo Reforms

Florida Regulator: Insurers Can Offer Roof Deductibles

Expansion Plans for Fort Myers Airport

Guide to Buying and Selling in Southwest Florida

Market Summaries

Florida Market Update in 4 minutes

Naples mid-year Market Report

Sales Resemble Pre-Pandemic — But Not Pricing & Inventory

- Andrew Oliver, M.B.E., M.B.A.

Real Estate Advisor

Andrew.Oliver@Compass.com

www.TheFeinsGroup.com

www.OliverReportsFL.com

m: 617.834.8205

———-

800 Laurel Oak Drive, Suite 400, Naples, FL 34108

———-

Licensed in Massachusetts

www.OliverReportsMA.com

If you – or somebody you know – are considering buying or selling a home and have questions about the market and/or current home prices, please contact me on 617.834.8205 or Andrew.Oliver@Compas