Hello sub 3% Mortgages – again

This week’s drop below 3% – again – reminded me that the only one thing more fraught than commenting on mortgage rates is trying to predict where rates are headed. (see below for some of my posts about mortgage rates.)

After rising steadily from 2.65% at the beginning of the year to 3.18% by the end of March, the 30-year Fixed Rate Mortgage (FRM) has backed off again and this week the rate dropped back under 3%.

Freddie Mac weekly survey

Mortgage spread over 10-year Treasury yield

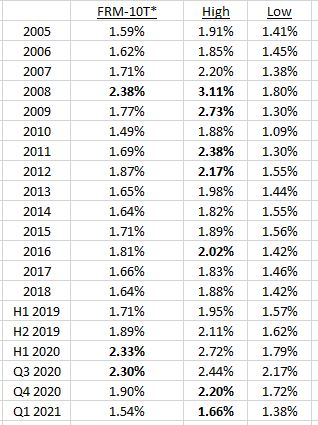

Conventional mortgages are sold to Fannie Mae and Freddie Mac who bundle them into pools and sell them to investors. Because of the greater risk investors require an extra yield – spread – over what they can earn by buying US 10-year Treasury Notes.

Since 2005 this spread has mostly been in the 1.5-1.8% range with two major exceptions: the Great Recession and the Pandemic. The table below shows that the average spread in 2008 was 2.38% and reached over 3% at one point.

Similarly, in 2020 the spread averaged 2.3% in the first 9 months and reached a high of 2.7%.

As financial markets returned to more normal conditions so this spread dropped back into the historic range and has been at the low end this year, in part because the Federal Reserve continues to be a buyer of the pools of mortgage-backed securities (MBS).

The next chart shows the course of the spread since the beginning of 2020:

Comment

There are two basic underlying economic assumptions: increased Government spending will need to be financed by buyers of US Treasuries and these buyers will demand higher yields to attract them; and at the same time this increased spending – particularly at a time of rebounding economic activity where shortages and supply chain problems are already being felt – will lead to an increase in inflation, which will also drive up the yield investors seek to finance the spending.

There is an alternative economic philosophy known as Modern Monetary Theory. You can read about it by clicking What is Modern Monetary Theory?”

A short summary reads:

“While businesses and households must come up with the cash to keep up with their bills, the United States can pay any debt it has because we can always print money. So too for Canada, Japan, the United Kingdom, and any government that does three things:

-issues its own currency

-allows its exchange rate to float

-avoids borrowing funds that require repayment in a foreign currency

While eurozone members and most emerging-market countries don’t meet those three criteria, a monetarily sovereign government, such as the United States, can’t be forced into insolvency.”

While MMT has been a theory until now, there are some whoa argue that we are actually implementing some form of MMT as the US faced an even larger Budget deficit which needs to be financed with the Federal Reserve forecasting that this will not lead to inflation.

We shall see.

Meanwhile, I will repeat two of my mantras of recent years. Mortgage rates remain very cheap by any historical standard, and the simple law of supply and demand will continue to determine home prices. We continue to see fierce bidding wars for the limited supply on the market.

Past articles:

2021

Goodbye sub 3% mortgages

It was only last July that the 30-year Fixed Rate Mortgage (FRM) dropped below 3% for the first time and this week it moved back above 3% again, following the direction of the 10-year Treasury Note (10T).

Are mortgage rates about to rise?

Following the Georgia Senate election results, which gave control of the Senate to the Democrats, along with the House of Representatives and the White House, the yield on the 10-year Treasury Note (10T) – the most sensitive to increased Government spending – jumped from 0.93% on Monday to 1.13% on Friday, based upon the expectation that increased Government spending would lead to more borrowing which would need higher interest rates to attract investors.

2020

Mortgage Markets Return to Normal

As financial markets have calmed down, the spread between FRM and 10T has been falling steadily since the middle of the year and is now within the normal range again.

Mortgage rates: Another new low

The 30-year Fixed Rate Mortgage (FRM) as reported by Freddie Mac dropped to yet another new low this week of just 2.72%.

Mortgage Rates: another Head Fake or Early Warning?

Back in June I wrote Mortgage rate head fake, when mortgage rates jumped but only very briefly.

On Wednesday this week I wrote: “In normal times, the 30-year Fixed Rate Mortgage (FRM) is priced based upon the extra yield investors require over and above that which can be received on the US 10-year Treasury Note (10T). In recent years that extra yield – spread – has averaged 1.7%.

Mortgage rates dip below 3% – where next?

The 30-year Fixed Rate Mortgage dropped below 3% this week but the spread over 10-year Treasuries remains elevated.

Mortgage rates are rising – and that’s good news

The reason that the rise in interest rates this week is good news is that it is an indication that markets are at least starting to return to normal. We are not going to see mortgage rates fall into line with the 10T + 1.7% formula (implying a FRM of 2.6%) because in times of economic stress the formula changes slightly to 10T +1.7% + a risk premium.

Mortgage rates hit all-time low – again

Remember late March when the 30-year Fixed Rate Mortgage jumped more than 1% in one day when the financial markets were in disarray? The multiple actions taken by the Federal Reserve have created both liquidity and confidence and the impact has been dramatic in both the stock market and the conventional mortgage market.

A Calmer Mortgage Market

The most likely outcome is that, as the US economy rebounds later this year, the yield on 10T will rise and the risk premium demanded by buyers of MBS decline, narrowing the spread. But there are no models for this pandemic, and no forecasts – just guesstimates at this stage

Mortgage rates after the collapse of bond yields

My best guess – and at this stage it is a guess – is that in time, when we know the extent of the economic slump and the pace of recovery, interest rates will raise again. Could the FRM reach 3%? Yes. Will it? Ask me again in a couple of weeks.

Andrew Oliver

Sales Associate | Market Analyst | DomainRealty.com

Naples, Bonita Springs and Fort Myers

Andrew.Oliver@DomainRealtySales.com

m. 617.834.8205

www.AndrewOliverRealtor.com

www.OliverReportsFL.com

Andrew Oliver

Market Analyst | Team Harborside | teamharborside.com

REALTOR®

Sagan Harborside Sotheby’s International Realty

One Essex Street | Marblehead, MA 01945

m 617.834.8205

www.OliverReportsMA.com

Andrew.Oliver@SothebysRealty.com

Sotheby’s International Realty® is a registered trademark licensed to Sotheby’s International Realty Affiliates LLC. Each Office Is Independently Owned and Operated

“If you’re interested in Marblehead, you have to visit the blog of Mr. Andrew Oliver, author and curator of OliverReports.com. He’s assembled the most comprehensive analysis of Essex County we know of with market data and trends going back decades. It’s a great starting point for those looking in the towns of Marblehead, Salem, Beverly, Lynn and Swampscott.”